How Much House Can I Afford in Raleigh NC 2026

How Much House Can I Afford in Raleigh NC 2026?

It’s one of the most important—and misunderstood—questions for homebuyers in Raleigh, Wake County, and across the Triangle.

Most buyers start with a price.

But affordability isn’t just about the home price.

It’s about how your income, debt, down payment, and mortgage rate work together.

What Determines How Much House You Can Afford?

Your affordability is based on four key factors:

- Your income

- Your existing debt

- Your down payment

- Your mortgage interest rate

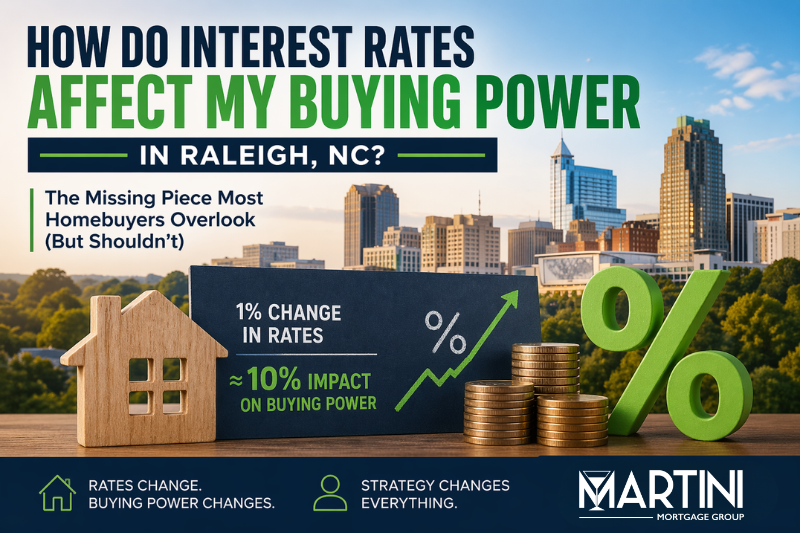

Of these, the variable that changes most often—and impacts the most—is the rate.

If you haven’t already, it’s worth understanding how interest rates affect your buying power in Raleigh NC.

The Role of Mortgage Rates in Affordability

Even a small change in rates can significantly impact your monthly payment.

That means:

- Higher rates reduce what you can afford

- Lower rates increase what you can afford

But that’s only part of the story.

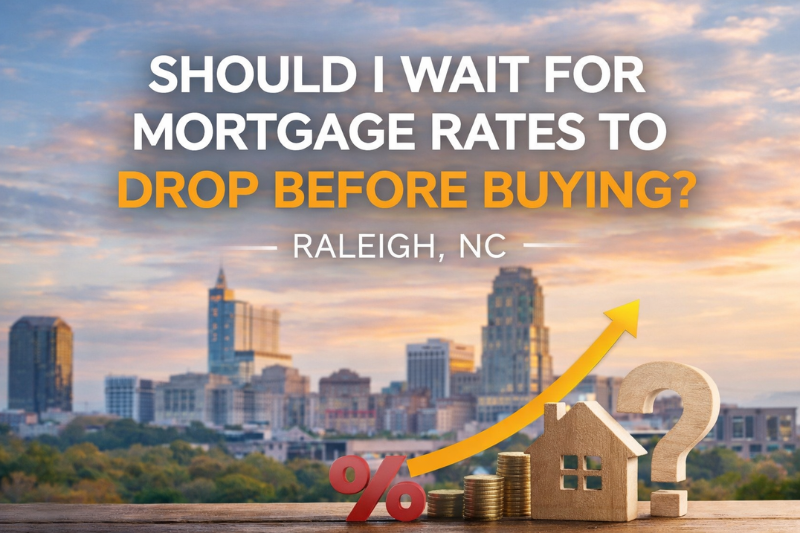

The Raleigh Market Factor

In Raleigh, North Carolina, affordability doesn’t exist in a vacuum.

When rates drop:

- More buyers qualify

- Demand increases

- Competition rises

When rates are higher:

- Fewer buyers are active

- Sellers may be more flexible

- Negotiation opportunities improve

If you’re trying to decide whether to act now or wait, this breakdown of should I wait for mortgage rates to drop before buying can help.

What Monthly Payment Should You Be Comfortable With?

A better question than “how much can I afford” is:

“What payment am I comfortable with?”

Before settling on a number, it is worth understanding what AI misses about mortgage affordability in Raleigh NC — the five local costs no chat window captures that change what comfortable actually means in Wake County.

A comfortable payment considers:

- Your lifestyle

- Future financial goals

- Savings and reserves

- Risk tolerance

The Difference Between Approval and Affordability

Just because you’re approved for a certain amount doesn’t mean you should spend it.

Approval = what a lender allows

Affordability = what fits your life

The smartest buyers focus on sustainable payments, not maximum approval.

That sustainable number works best as a boundary set in advance. See how a defined mortgage payment range Raleigh NC narrows the search before the first showing.

How to Strengthen Your Buying Position

Affordability isn’t just about numbers.

It’s about preparation.

Buyers who go in fully underwritten—with a Same-As-Cash Mortgage Approval can:

- Compete more effectively

- Move faster

- Negotiate stronger

What Most Raleigh Buyers Get Wrong

Many buyers wait for the “perfect” moment.

Lower rates.

Lower prices.

Less competition.

But markets don’t align perfectly.

Waiting can improve one variable and worsen others.

If you want to understand that tradeoff, review:

TL;DR — How Much House Can You Afford in Raleigh?

- Affordability depends on income, debt, down payment, and rates

- A 1% rate change can shift buying power ~10%

- Lower rates increase competition

- Higher rates can create an opportunity

- Your comfort level matters more than your max approval

Frequently Asked Questions About Affordability in Raleigh, NC

How much house can I afford in Raleigh NC 2026?

The amount you can afford depends on your income, debt, down payment, and current mortgage rates. In Raleigh, even a small change in interest rates can significantly impact your buying power and the price range you qualify for.

What monthly payment should I be comfortable with?

A better approach than focusing on price is to determine a payment that fits your lifestyle, financial goals, and savings plan. Just because you are approved for a higher amount doesn’t mean it’s the right decision.

Do lower mortgage rates mean I can afford more?

Yes, lower rates can increase your buying power. However, in markets like Raleigh, lower rates also tend to increase buyer demand and competition, which can offset the advantage.

Does getting pre-approved tell me exactly what I can afford?

Pre-approval shows what a lender may allow, but it does not always reflect what is comfortable or sustainable for you. Strategy and long-term planning matter just as much as approval.

Should I wait to afford more house?

Waiting may improve affordability if rates drop, but it can also increase competition and reduce negotiating power. The better decision depends on your financial position and timing—not just market conditions.

What’s the Right Number for You?

There’s no universal answer.

But there is a smarter way to approach it.

If you’re buying in Raleigh, NC, the goal isn’t to guess your number.

It’s to understand how your numbers, the market, and your strategy align.

At Martini Mortgage Group, we take a fiduciary, strategy-first approach to help you make that decision with clarity—not pressure.