Martini Buyer Guide (Your Complete Guide to Buying a Home)

Are you ready to transform your dream of homeownership into a reality? The Martini Buyer Guide is your essential resource for navigating the intricate world of Raleigh real estate with confidence and clarity. This guide provides the insights and strategies to make informed decisions and secure your dream home.

What You’ll Learn Inside the Martini Buyer Guide:

Why Owning a Home is One of the Best Investments You Can Make: Discover the long-term financial benefits of homeownership, from building equity to leveraging tax advantages. Understand how working with a trusted Raleigh mortgage lender like Martini Mortgage Group can help you maximize your investment.

The Power of Securing Your Loan First: Learn how flipping the script by securing your loan before house hunting gives you a competitive edge in the Raleigh real estate market. Martini Mortgage Group’s innovative loan-first approach ensures you’re well-prepared, reducing stress and increasing your buying power.

Debunking Homebuying Myths: Get the facts straight about common misconceptions, such as the need for a 20% down payment, the financial comparison between renting and buying, and how student loans affect your mortgage approval. Logan Martini’s expertise as a Raleigh mortgage broker sheds light on these critical topics.

Tailoring Your Homebuying Journey: Understand why a one-size-fits-all approach doesn’t work in real estate. Martini Mortgage Group specializes in crafting personalized mortgage strategies that fit your unique financial situation, ensuring your homebuying journey is smooth and successful.

Working with the Right Real Estate Agent: Discover the importance of choosing a hyper-local real estate expert who understands the nuances of the Raleigh market. Martini Mortgage Group can connect you with the best real estate agents, helping you find the perfect home in the right neighborhood.

Prioritizing Your Must-Haves, Nice-to-Haves, and Dream Features: Learn practical tips on how to prioritize your home search, balancing your budget with your long-term goals. Kevin Martini’s insights will guide you in making decisions that align with your financial future.

Table of Contents for Martini Buyer Guide

Martini Buyer Guide Preface

Ever had that “aha!” moment? That sudden spark of clarity where everything clicks into place? Think of this Martini Buyer Guide as your light bulb moment for home buying—the beginning of turning that dream home in your mind into a reality.

Picture it now: the home you’ve always imagined. Maybe it’s a sprawling yard for summer barbecues or a cozy nook by the window where you can curl up with a good book. But here’s the thing—turning that dream into reality takes more than just imagination. It requires planning, strategy, and a clear vision of what’s to come. Think of it like baking your favorite cake; you wouldn’t start mixing ingredients without a recipe. Buying a home is no different—you need a solid blueprint.

Why is this so important? Well, just like you wouldn’t start building a puzzle without first looking at the picture on the box, buying a home works best when you have a clear plan in place. This blueprint isn’t just a nice-to-have; it’s essential. It’s the difference between a smooth, successful home-buying experience and a stressful, overwhelming one.

Here’s a little-known fact: Many eager homebuyers jump headfirst into house hunting, seduced by charming porches and sparkling countertops. But soon, they hit a wall—whether it’s unexpected costs piling up or realizing they’ve fallen in love with a home that’s just out of reach. The heartbreak is real, but the good news is it’s completely avoidable with the proper steps.

So, what’s the magic formula? Start with the numbers before you start dreaming about paint colors or envisioning your future holiday gatherings. It’s like checking your pantry before you bake—you wouldn’t want to get halfway through a recipe only to realize you’re missing key ingredients. Knowing your budget, understanding your mortgage options, and planning for all the associated costs might not sound glamorous, but trust me, this is the secret sauce to home buying.

Remember, a home is more than just bricks and beams. It’s a foundation for memories, a space for growth, and a haven of comfort. Your perfect home should fit your life in every way—both the fun, exciting parts and the serious, practical ones like your finances.

Here’s something to keep in mind: The real value of a home isn’t just in its market price. It’s in the memories you’ll create, the security it offers, and the peace of mind that comes from knowing you’ve made a sound investment. And that peace of mind? It starts with a rock-solid plan.

In the pages ahead, we’ll break it all down for you—clear, simple, and straightforward. Whether you’re a seasoned pro or a first-time homebuyer, with the Martini Buyer Guide, you’ll have a clear path forward. You’ll be ready to navigate the home-buying journey with confidence, armed with the knowledge and strategies you need to make your dream home a reality.

In addition, you have full confidential access to a mortgage strategist with the Martini Mortgage Group by simply dialing (919) 238-4934. Whether you need personalized advice or just want to clarify any part of the process, our experts are here to support you every step of the way.

Homebuyer Opportunities Today (Winter 2025)

It’s no secret that the past year has been tough for homebuyers. But here’s the good news: the market is shifting, and that shift brings opportunities for Raleigh homebuyers.

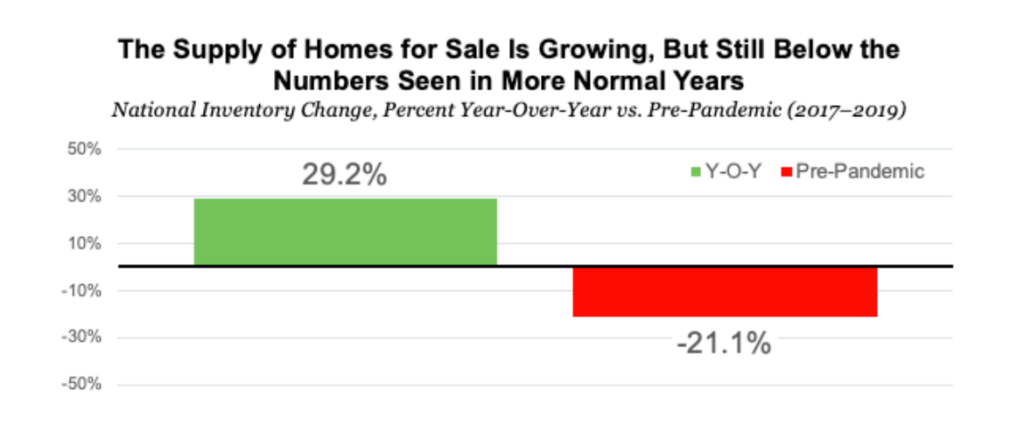

1. More Choices Than Before

Inventory is up over 29% compared to last year, according to Realtor.com. That means you’re more likely to find a home that truly feels right for you. But while there are more options, it’s not a free-for-all—inventory is still 21% lower than pre-pandemic levels. So, the key is being ready when the right home pops up.

2. New Homes Are on the Menu

Not finding what you want in existing homes? Builders have been busy. Nearly 29% of homes on the market today are new builds, per Census and NAR data. And don’t worry—this isn’t a case of overbuilding. Builders are catching up after years of underproduction, and many of these homes are designed with affordability in mind. Adding new builds to your search could expand your options in a big way.

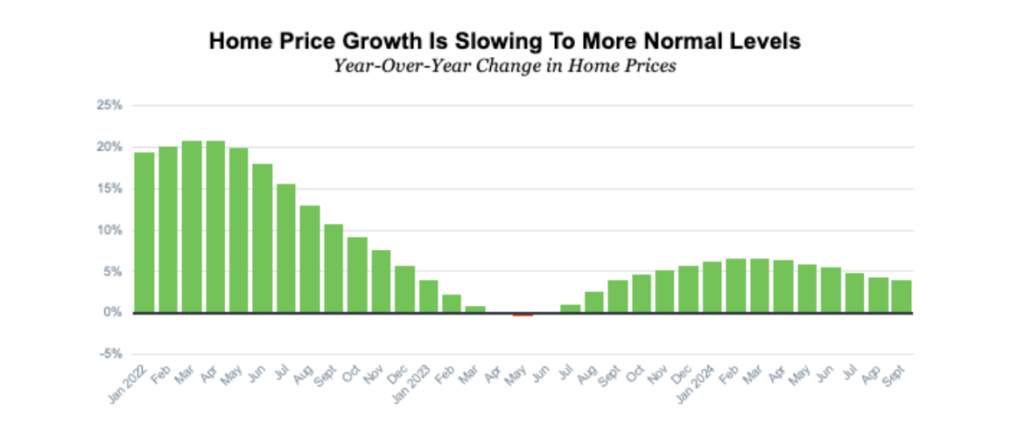

3. Prices Are Cooling Down

Finally, after years of skyrocketing home prices, we’re starting to see them moderate. This is a moment to take a breath and know the market might be tilting a little more in your favor.

So, what does this mean for you? It means opportunity—if you’re ready. A shifting market favors the prepared buyer. Let’s make sure you’re positioned to take advantage.

Finally, some sanity in the housing market. With supply catching up and demand easing, home prices aren’t sprinting out of reach anymore—they’re jogging at a steady, manageable pace. Let’s be clear, though: prices aren’t dropping. They’re just growing in a way that doesn’t make you feel like you’re chasing a runaway train. This is your chance to step into the market without the whiplash of the price surges we’ve seen in the past. Ready to claim your home while the timing’s on your side?

Raleigh Mortgage Broker Logan Martini

Things to Know About Credit

Your Credit Scores Vary by Industry:

Not all credit scores are created equal. When you apply for a mortgage, mortgage lenders don’t use the same score that a car dealership or a credit card company does. Mortgage lenders assess your credit with greater scrutiny, using a tailored score specific to home loans. This distinction is vital because it ensures lenders see the full scope of your financial responsibility. Be aware of this difference—it will prepare you for the mortgage process and prevent surprises.

Why Free Credit Scores Won’t Give You the Complete Picture

Many services offer a free credit score, but they won’t tell you everything you need to know when it comes to securing a mortgage. These scores often overlook key factors that mortgage lenders take into account. Think of these free scores as a rough estimate—useful, but not precise. If you want to know exactly where you stand for a home loan, you need a specific mortgage credit pull. Only then will you see the true number that a mortgage lender considers for your home loan qualification.

7 Reasons to Own Your Home

Owning a home isn’t just about having a place to live—it’s about building a foundation for your financial future and creating a space that’s truly yours. Here are the top reasons why homeownership is one of the smartest, most rewarding investments you can make:

- Appreciation: Real estate has historically demonstrated long-term, stable growth in value, making it a reliable hedge against inflation. By owning a home, you’re investing in an asset that, over time, has the potential to significantly increase in value.

- Equity: When you pay rent, that money is gone forever. But with a mortgage, each payment contributes to building your equity—your ownership interest in the home. Over time, as you pay down your mortgage and your home potentially appreciates in value, your equity grows, adding to your personal wealth.

- Tax Benefits: The U.S. Tax Code offers several benefits to homeowners who itemize deductions on their federal tax return. You can deduct the interest paid on your mortgage, property taxes (up to $10,000 according to current tax law), and certain costs associated with buying a home. These tax advantages can make homeownership more affordable and financially beneficial. Be sure to consult your tax professional to determine if itemizing is advantageous for your situation.

- Savings: Building equity in your home is like creating a built-in savings plan. When the time comes to sell, you can typically exclude up to $250,000 of gain ($500,000 for a married couple) from federal income tax, assuming you meet certain IRS qualifications. This exclusion means more money in your pocket when you cash out on your investment.

- Predictability: Unlike rent, which can increase annually, a fixed-rate mortgage provides consistent monthly payments. Over time, as your income grows, your mortgage payment becomes a smaller percentage of your overall expenses, potentially freeing up more of your budget for other goals. Just keep in mind that property taxes and insurance costs may rise, but your principal and interest payments will remain steady.

- Freedom: Owning your home gives you the freedom to make it truly yours. Want to paint the walls a bold new color? Go for it. Thinking of adding a deck or upgrading the kitchen? It’s your call. Your home is a canvas for your personal style and lifestyle, offering you the freedom to create a space that reflects your tastes and needs.

- Stability: Homeownership offers more than just financial stability; it provides social and community stability as well. Staying in one place for several years allows you and your family to build long-lasting relationships within the community. It also offers children the benefit of educational and social continuity, which can be invaluable for their development.

How to Start the Home-buying Process: Flipping the Script

Have you ever heard the saying, “Put the cart before the horse?” Well, in the world of home-buying, sometimes it’s actually a smart move! Most folks start with a home search, picturing the white picket fence, the cozy fireplace, and maybe even the dog running in the yard. Then, they think about the money part. But here’s a thought: What if you flipped that story?

The Undeniable Benefits of the Loan-First Tactic: By securing your home loan first, you’re getting a golden ticket. It’s like getting a backstage pass at a concert. You’re not just in the door; you’re ahead of the game. Why?

- You know exactly what you can afford, so there’s no heartbreak over homes out of your range.

- Sellers will take you seriously. Imagine two buyers: one with a loan ready and one without. Who do you think a seller would trust more?

- Less stress. Period.

The Power of Being Ahead: Thinking loan-first isn’t just about money. It’s about feeling confident and in control. It’s about holding a sense of power when you walk into a home negotiation. With your loan ready, you’re in control: no waiting on loan approvals while your dream home gets snagged by someone else. You’ll have peace of mind knowing what you can afford, and no surprise costs will shake up your finances. Plus, it feels good to be prepared. Imagine walking into a store and knowing exactly how much you can spend. No surprises. No disappointments. That’s the magic of the loan-first approach.

Homebuying Myths

Myth #1: You Need to Save Up for a 20% Down Payment

When you’re planning to buy your first home, the idea of saving up for all the associated costs can feel overwhelming—especially when it comes to the down payment. You might have heard that you need to put down 20% of the home’s price at closing. This is a common and costly misconception.

Sure, putting down 20% to avoid mortgage insurance is a smart move if your finances allow it. But let’s set the record straight: it’s not a strict requirement. In fact, many homebuyers successfully navigate the path to homeownership with a much lower down payment. Remember that the market isn’t waiting for you while you’re diligently saving for that 20%. Home prices continue to rise, and the cost of mortgage insurance often pales compared to the potential cost of missing out on today’s market opportunities. In some cases, it’s better to act now with a smaller down payment than to delay and lose out on the market’s momentum.

Here’s the good news: a 20% down payment is typically not required. This means you might be much closer to achieving your homebuying dream than you realize.

Myth #2: Renting Makes More Financial Sense

You might have heard from some people—your landlord included—that renting is the smarter financial move. But when you look at the bigger picture, owning a home still offers significant advantages, particularly when it comes to building long-term wealth.

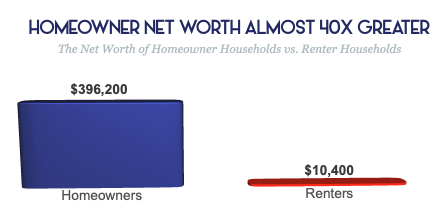

Consider this: every three years, the Federal Reserve releases the Survey of Consumer Finances (SCF), which compares the net worth of homeowners and renters. The latest report shows a staggering difference—homeowners have an average net worth nearly 40 times greater than that of renters. Specifically, the net worth of a typical homeowner is $396,200, while a renter’s is just $10,400.

One key reason for this wealth gap is that homeowners build equity over time. As your home appreciates in value and you make your monthly mortgage payments, your equity—and, therefore, your net worth—grows. In essence, your mortgage payments act as a form of forced savings, which can yield significant returns when you eventually sell your home. Renters, on the other hand, don’t see any financial return on the money they pay in rent each month.

Renters miss out on the wealth that comes from rising home values and the equity that builds with every mortgage payment. While homeowners are growing their financial future, renters remain stuck in place. Some renters hesitate, fearing the commitment of a mortgage, but here’s the harsh truth: when you rent, you’re already paying a mortgage—just not your own. It’s your landlord’s wealth you’re building, not yours.

Mortgage Strategist and Raleigh Mortgage Broker Logan Martini

Owning a home isn’t just about having a place to live—it’s about investing in your future and growing your personal wealth. While renting might seem easier in the short term, the long-term benefits of homeownership far outweigh the perceived advantages of renting.

Myth #3: My Student Loans Mean I Won’t Get Approved for a Mortgage

If you’re carrying student loans and dreaming of buying a home, you might be worried that your debt will hold you back. Do you need to pay off all your loans before even considering a home purchase? The answer is no—you don’t have to delay your homeownership goals because of student debt.

Many first-time buyers share the concern that student loans will prevent them from getting approved for a mortgage. However, it’s important to know that even with student loan debt, buying a home may be more achievable than you think.

Yes, You Can Qualify for a Home Loan Even If You Have Student Loans.

According to a report by the National Association of Realtors (NAR), 38% of first-time homebuyers had student loan debt, with a median amount of $30,000. This statistic highlights that many people with student loans successfully navigate the path to homeownership.

Homebuyers with student loans can still qualify for a mortgage—you don’t need to be entirely debt-free to buy a home. When assessing your eligibility, we look at the overall debt picture, including student loans. Having both student loans and a mortgage is entirely possible. There are several mortgage programs specifically designed to accommodate your financial situation, allowing you to achieve homeownership without the need to pay off all your debts first.

Mortgage Strategist and Raleigh Mortgage Broker Logan Martini

Your student loans don’t have to be an obstacle to buying a home. With the right guidance and mortgage strategy, homeownership can be within your reach, even if you’re still managing student debt.

Crafting Success: Tailoring Strategies That Fit You

Have you ever worn a shirt or dress that’s either too tight or too baggy? Not comfortable, right? Much like our clothes, when it comes to making big decisions about our homes and money, we need a fit that’s just right. A fit that feels… well, tailored to us.

Every Puzzle Piece is Unique: You are No Exception

Think of your financial journey as a giant puzzle, each piece unique. Just as no two puzzle pieces are identical, no two financial stories are the same. Whether it’s your first or third home, expanding or downsizing, your story is yours alone.

At Martini Mortgage Group, we believe in celebrating that uniqueness. Instead of offering a one-size-fits-all plan, we sculpt a mortgage strategy as unique as you. How? By listening—really listening—to your dreams, worries, and future plans.

The Craft Behind Tailored Success

Ever seen a master tailor at work? With careful hands, keen eyes, and unmatched expertise, they turn a piece of cloth into a masterpiece. Similarly, Martini Mortgage Group becomes the master tailor of your mortgage journey.

But it’s not just about numbers. It’s about understanding. Tailoring isn’t just for clothes. It’s for dreams. It’s for your future. It’s for success stories waiting to be written. And with a partner like Martini Mortgage Group, you’re not just another number; you’re an individual with dreams ready to be crafted into reality.

Unlocking the Language of Homebuying: Key Terms to Know When Getting a Mortgage

Understanding the key terms involved in home-buying is essential for making informed decisions. Each term represents a critical aspect of your journey, and grasping their meanings will empower you to navigate the process confidently.

Affordability

Affordability isn’t just a number—it’s the foundation of your home-buying strategy. It’s a measure of whether your income aligns with the most recent home prices and mortgage rates, ensuring that your dream home fits comfortably within your financial reality. When you know your affordability, you’re not just house hunting; you’re making a strategic move toward a home that complements your lifestyle and long-term goals.

Appraisal

An appraisal guarantees that you’re paying a fair price for your home. This third-party report, conducted by a qualified professional (a.k.a. an appraiser), determines the true value of the property, giving both you and the lender confidence that the investment is sound. With an accurate appraisal, you’re stepping into your purchase with the certainty that you’re not overextending your finances, and the lender is assured that the home is worth every penny of the loan.

Closing Costs

Closing costs are the final step in securing your home—the detailed breakdown of fees that ensures every aspect of the transaction is completed with precision. These costs include points, taxes, title insurance, and more, all of which are crucial for a seamless transfer of ownership. With a clear understanding of closing costs, you’re equipped to close the deal with no surprises, knowing exactly where your money is going.

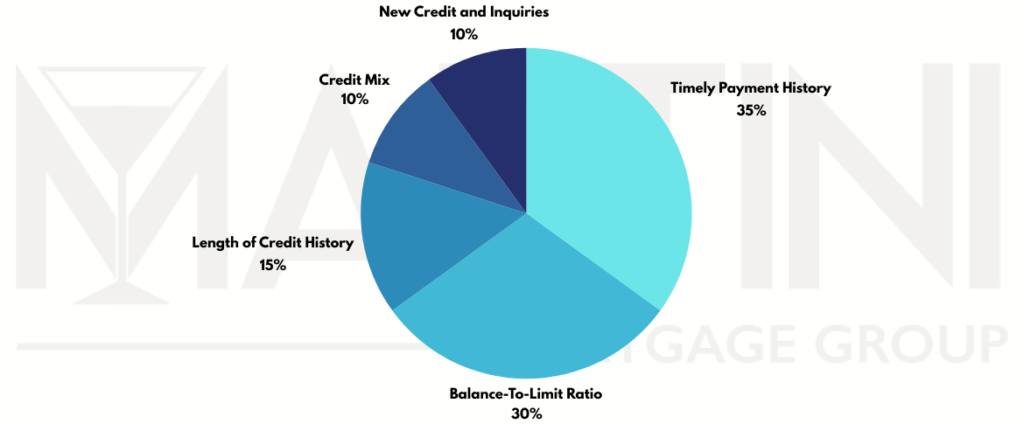

Credit Score

Your credit score is your financial fingerprint—a unique number that reflects your borrowing history and financial behavior. In the world of mortgages, this score, ranging from 300 to 850, is a critical factor that lenders use to assess your likelihood of repaying debts. It’s more than just a number; it’s the key that unlocks the terms of your mortgage. A strong credit score doesn’t just get you in the door; it positions you for the most favorable mortgage terms, giving you a significant advantage in your home-buying journey.

It’s important to note that your credit score isn’t one-size-fits-all. Different credit score models are used depending on the type of credit you’re applying for—whether it’s a car loan, credit card, or mortgage. For instance, a car loan uses an installment model, while a credit card application uses an unsecured credit score model. Unfortunately, free credit score services often provide scores that don’t accurately reflect the mortgage-specific model. That’s why it’s essential to work with a mortgage strategist with the Martini Mortgage Group so they can provide you with the correct credit score and guidance tailored to the mortgage process.

Down Payment

Your down payment is your initial investment in your future home. Typically ranging from 3% to 20%+ of the purchase price, this payment plays a crucial role in determining your mortgage terms and monthly payments. But with options like 0% down programs available, Martini Mortgage Group works with you to explore every possibility, ensuring your down payment fits your financial situation and helps you step confidently into homeownership.

Equity

Equity is your stake in your home—literally, the portion of your home’s value that you own outright. It’s what you build as you pay down your mortgage and as your home appreciates over time. Equity isn’t just a number on paper; it’s a powerful financial tool that grows with you, offering opportunities for future investments, refinancing, or simply providing peace of mind that you’re building wealth with each mortgage payment.

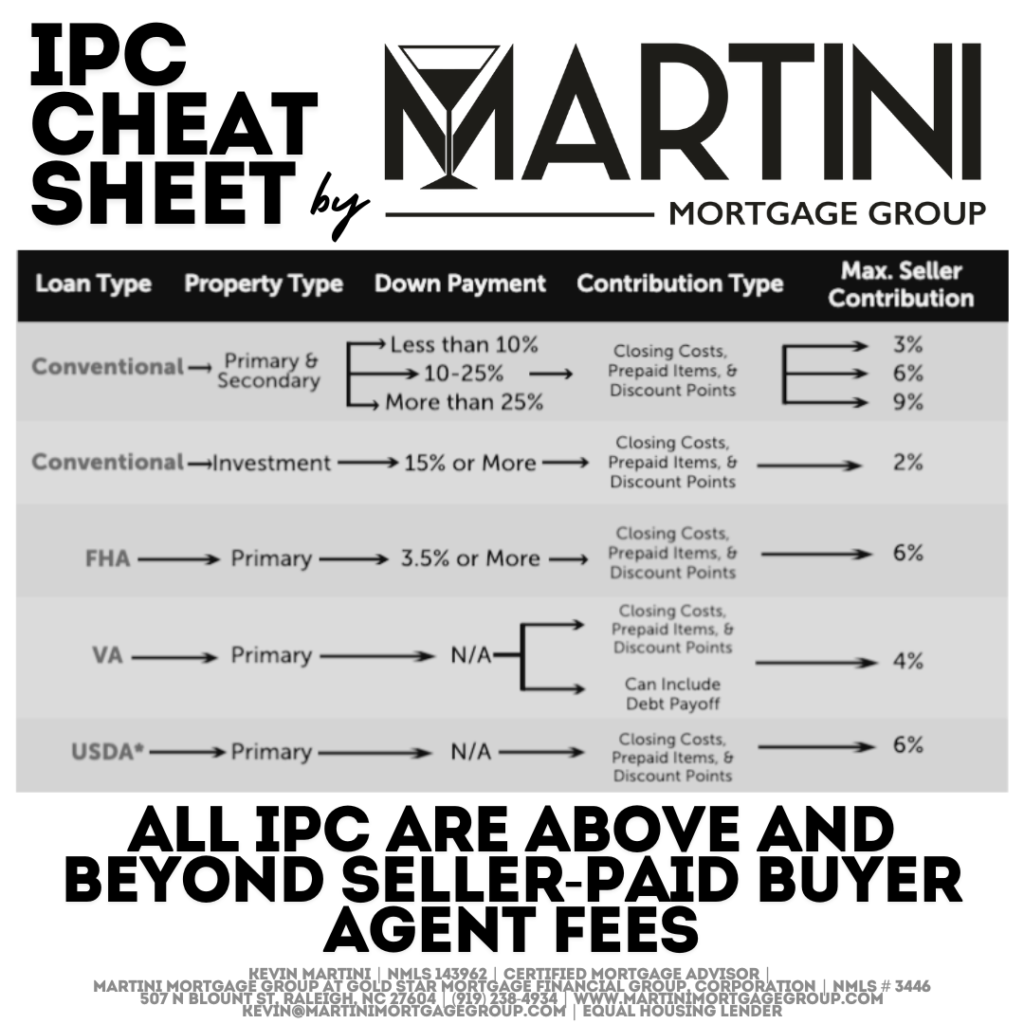

Interested Party Concessions

Interested Party Contributions, or IPCs, are financial contributions made by parties involved in the home-buying transaction other than the borrower. These parties can include sellers, builders, or real estate agents, and their contributions can be used to cover specific costs such as closing costs, prepaid items, and discount points. However, it’s important to note that IPCs cannot be applied toward the borrower’s down payment. Additionally, there are limits to how much can be contributed, which are determined by the property’s sale price or appraised value, and these limits can vary depending on the type of loan and lender policies. Understanding IPCs is crucial as they can significantly impact the affordability and terms of your mortgage.

Mortgage

A mortgage is more than just a loan; it’s the financial partnership that turns your homeownership dreams into reality. Using your home as collateral, this loan represents the amount you borrow to purchase your house, typically the price of the home minus your down payment. With the right mortgage, structured by Martini Mortgage Group, you’re not just borrowing money—you’re creating a financial plan that supports your long-term goals and lifestyle.

Mortgage Rate

Your mortgage rate is the cost of borrowing money to buy your home—the interest rate that defines your monthly payments and overall affordability. As mortgage rates fluctuate, understanding how they impact your payments is crucial. Martini Mortgage Group helps you secure the most favorable rate possible, ensuring your mortgage fits seamlessly into your budget and allowing you to enjoy your new home without financial strain.

Same-As-Cash Approval Package by Martini Mortgage Group

A “Same-As-Cash” Approval Package by Martini Mortgage Group is more than just a standard pre-approval letter—it’s a powerful tool that provides the seller with clear evidence of your financial capability and commitment. This package confirms both your willingness to purchase and your ability to do so, ensuring the transaction is frictionless and will close on time. It offers sellers the certainty they crave, making your offer stand out in a competitive market.

A Real Estate Agent Does More Than You May Realize

A great buyer’s agent isn’t just a guide—they’re your secret weapon. They’ll uncover the perfect home, craft an offer that stands out, negotiate terms that protect your interests, and ensure every step to closing feels seamless. The right agent turns homebuying from overwhelming to empowering, giving you the confidence to claim the keys to your future.

Certified Mortgagr Advisor & Raleigh Mortgage Broker Kevin Martini

When it comes to buying a home, the role of a real estate agent is far more significant than many people realize. Real estate isn’t just local—it’s hyper-local. A real estate agent specializing in one neighborhood may not have the same expertise in another part of the same town. This is where the proven tactic of securing your home loan first reveals another hidden benefit: it provides not only cost and price clarity but, most importantly, certainty. With a clear budget and a defined location, Martini Mortgage Group can complement your journey by recommending a real estate professional who excels in the niche market you wish to call home.

Your real estate agent, alongside your mortgage strategist at Martini Mortgage Group, will guide you through every step of the home buying process, always looking out for your best interests. The real estate agents the Martini Mortgage Group refers to are experts in smoothing out the complexities and alleviating the bulk of the stress from what is likely the largest purchase of your life. And that’s exactly what you need—and deserve.

In a recent survey, an overwhelming majority agreed that an agent is a crucial part of the home buying process. A staggering 87% of respondents believe that “a real estate agent is an essential, trusted advisor for a homebuyer.” Moreover, 93% agreed that “it would be very stressful to navigate the home buying process without a real estate agent.”

The real estate agents referred by Martini Mortgage Group are more than just transaction facilitators—they are specialists, educators, and negotiators. To best serve the families we work with, these agents must:

- Deliver Industry Experience: They bring a wealth of knowledge and expertise to ensure you’re making informed decisions.

- Provide Expert Local Knowledge: Their deep understanding of specific neighborhoods and market trends helps you find the perfect home in the right area.

- Explain Pricing and Market Value: They ensure you understand the true value of a property and help you make competitive offers.

- Review and Explain Contracts: They navigate the complexities of real estate contracts, protecting your interests every step of the way.

- Bring Negotiation Expertise: They skillfully negotiate on your behalf, striving to get you the best possible deal.

Additionally, these agents are vetted for their ability to adapt to market changes and keep you informed before and after the transaction.

When you work with Martini Mortgage Group, you’re not just getting a mortgage—you’re getting a team of trusted advisors, including top-tier real estate agents committed to making your homebuying experience as smooth and successful as possible.

Prioritizing Your Homebuying Essentials

The key to making a sound decision in any housing market is to stay sharply focused on your current needs and future goals. Equally important, resist the temptation to stretch your budget, even when purchasing power feels constrained. Prioritize long-term stability over short-term gains.

Certified Mortgage Advisor and Raleigh Mortgage Broker Kevin Martini

When searching for a home, it’s essential to distinguish between what’s necessary and what’s merely nice to have. The best way to do this is by creating a prioritized list of desired features that aligns with both your lifestyle and your financial reality.

As discussed earlier, the first step in your home buying journey is securing a “Same-As-Cash” Approval Package from Martini Mortgage Group. This powerful tool not only signals to sellers that you are serious and financially ready, but it also provides you with certainty—certainty about what you can afford and how much you can borrow. With this clarity, you can craft a home search strategy that’s both realistic and focused.

Here’s how to categorize and prioritize the features you want in your future home:

Must-Haves: These are the non-negotiables. If a house doesn’t have these features, it simply won’t work for you or your lifestyle. Think about the essentials like proximity to work or family, the number of bedrooms and bathrooms, or other critical aspects that are vital to your day-to-day living.

Nice-To-Haves: These are the features that would enhance your home experience but aren’t dealbreakers. They add value and comfort but aren’t essential. If a home meets all your must-haves and also includes some of these nice-to-haves, it’s a strong contender. Examples might include a second home office, a garage, or extra storage space.

Pie-in-the-Sky Features: Here’s where you can dream big. These features are the icing on the cake—luxuries that you don’t necessarily need but would love to have. If a home fits your budget and includes all your must-haves, most of your nice-to-haves, and even a few Pie-in-the-Sky Features, you’ve found something truly special. Think about features like a farmhouse sink, multiple walk-in closets, or a spacious backyard.

Once you’ve created and prioritized your list, share it with your real estate agent. They’ll help you refine the list further, coach you on how to stick to it and assist you in finding a home that meets your needs within your desired area.

Remember, staying focused on your essentials while remaining flexible with your nice-to-haves and dream features will guide you to a home that not only fits your budget but also aligns with your long-term goals.

Let’s Talk About Your Future

The Martini Buyer Guide has been carefully curated to provide essential information, offering a clear view of the critical facts you need to consider when deciding if homeownership is right for you. But just as every snowflake is unique, so is every homebuyer. Each person has different needs, concerns, and goals, and you must have all the correct information and education to make a confident decision.

Being in a state of uncertainty or doubt is something the Martini Mortgage Group aims to eliminate, and I’m sure you feel the same way, right?

The next step is to connect with a mortgage strategist at the Martini Mortgage Group and discuss your transition to homeownership. This isn’t about running your credit, gathering documents, or promoting our proprietary Same-As-Cash Approval Package. It’s about asking the right questions and providing the financial data you need to make an informed decision. And by the way, this conversation is confidential, judgment-free, and completely complimentary.

At the end of this discussion, you can confidently decide whether now is the right time for you to move forward, and if so, we’ll put a plan into motion. If it’s not the right time, that’s perfectly fine too—we’ll work together to create a strategy and timeline that fits your unique situation.