Understanding Key Factors That Affect Your Credit Score for a Raleigh Mortgage

When you’re looking to secure a mortgage in Raleigh, your credit score plays a pivotal role not just in determining your eligibility but also in influencing the interest rates you’ll be offered. At Martini Mortgage Group, led by the expert Certified Mortgage Advisor and Raleigh Mortgage Broker Kevin Martini, we understand that navigating through credit scores can be perplexing. Here’s an insightful look into the five critical factors that impact your credit score when applying for a Raleigh mortgage.

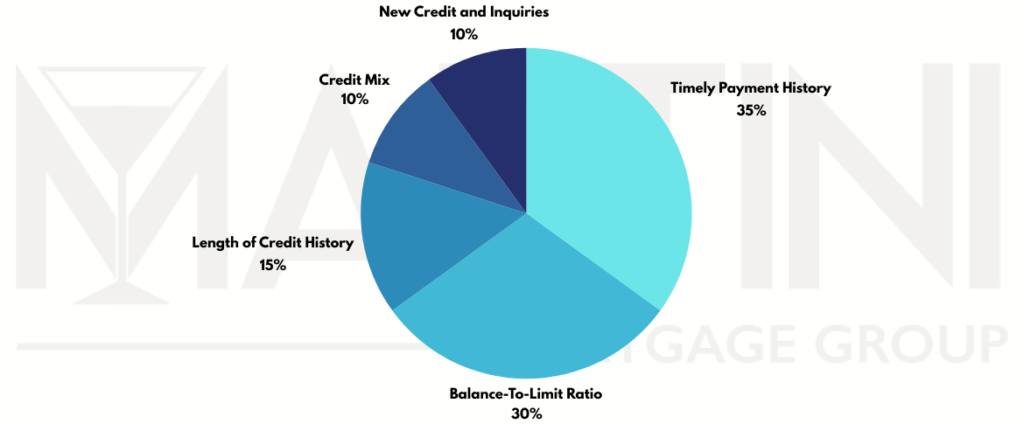

Timely Payment History

Your payment history is the most significant factor, affecting 35% of your credit score. In the realm of mortgage lending, it’s crucial to demonstrate a history of on-time payments. This shows potential Raleigh Mortgage Lenders that you’re a reliable borrower. Late payments can negatively impact your score, so it’s important to keep on top of your bills and ensure they are paid promptly.

Balance-To-Limit Ratio

Also known as your credit utilization ratio, this accounts for 30% of your credit score. It measures how much of your available credit you’re currently using. Raleigh mortgage lenders view a lower ratio favorably because it suggests that you’re not overextending yourself financially. Keeping your credit balances well below their limits is a smart strategy when preparing to apply for a mortgage.

Length of Credit History

Making up 15% of your credit score, the length of your credit history can add significant value to your credit profile. Raleigh mortgage lenders favor borrowers with longer credit histories as it provides more data to predict future behavior. This metric considers the age of your oldest credit account, your newest account, and the average age of all your accounts.

Credit Mix

The variety of credit types you manage accounts for 10% of your credit score. A mix of credit, such as revolving credit (like credit cards) and installment loans (like car loans or mortgages), can be beneficial. It shows lenders that you have experience managing different types of credit.

New Credit and Inquiries

Every time you apply for a new line of credit, it can cause a small, temporary drop in your credit score. This factor also contributes to 10% of your score. Frequent credit inquiries and new accounts can signal to lenders that you may be a higher-risk borrower, especially if you’re doing so over a short period.

The Kevin Martini Bottom Line

Understanding these key elements can enhance your creditworthiness and position you as an attractive candidate to lenders like the Martini Mortgage Group. Kevin Martini and his team at the Martini Mortgage Group, a premier Raleigh Mortgage Broker and Lender, are committed to helping you navigate the complexities of mortgage lending with ease. Whether you’re a first-time home buyer or looking to refinance, knowing what impacts your credit score is the first step toward securing favorable mortgage terms. Remember, a strong credit score opens doors to better rates and more flexible mortgage options.

For personalized guidance and expert advice, reach out to Kevin Martini at Martini Mortgage Group, your trusted Raleigh Mortgage Broker and Lender, ensuring your journey to homeownership is smooth and successful.