Are you thinking of buying a home in Raleigh? Before you dive into the process, it’s important to make sure that you are prepared for the journey. Here are three Martini Mortgage Group key things that you can do to get ready to buy a home in Raleigh or anywhere in the U.S. for that matter.

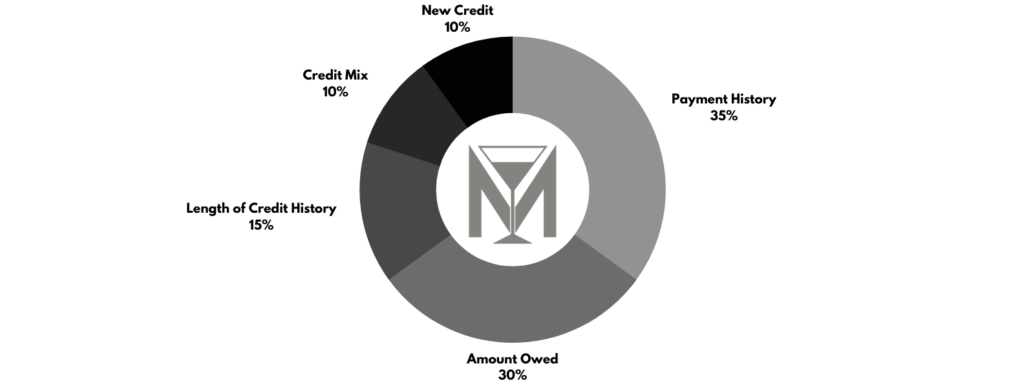

Prepare Your Credit

Before applying for a mortgage loan, it’s important to make sure your credit is in good shape. Mortgage lenders typically require a good credit history for you to qualify for a mortgage. This means having several credit cards and installment loans with payments made on time for the past two years, as well as making all rent payments on time during that period.

A good credit score will ensure that you have access to better mortgage rates and loan terms. You can look at your free credit report from the 3 major bureaus (Equifax, Experian, and TransUnion) once per year as well as order copies of your credit reports from each bureau through annualcreditreport.com. It’s important to review all of your reports closely and address any discrepancies or errors with the respective bureaus.

For more information about credit, check out: Martini Mortgage Podcast | Episode 167 | Freeze it and opt-out

Prepare Your Cashflow

It’s also important to take a close look at your income and expenses before beginning the process of buying a home in Raleigh.

Make sure that you understand how much money is coming in and going out each month, so that you can begin planning for what kind of house payment you can afford on top of any other existing debts or expenses. Knowing how much money is available for down payments and closing costs will help set realistic expectations about what kind of home you may be able to purchase in Raleigh.

It’s also important to make sure your debt-to-income ratio is not too high. Most lenders require that your total monthly debt payments (including the new mortgage payment) should not exceed 43% of your monthly income. If your debt-to-income ratio is higher than 43%, consider paying down some debts before taking out a new loan or try finding ways to increase your income.

Prepare Your Savings

Mortgage lenders typically require you to have a certain amount of savings in reserve in order to qualify for a mortgage. Your savings should be in your account for at least two months in order to qualify, and any large deposits will need to be explained and documented.

The amount of the required savings will vary based on the loan program that you choose. However, a good goal is to save enough for a 3%-5% down payment, plus 1-3 months of mortgage payment reserves.

For example, if your new mortgage payments will be $3,000 per month, you should probably aim to save approx. $9,000 plus the amount of your down payment.

Start budgeting now so that when it comes time to make an offer on your dream house, you’re prepared financially too!

Martini Mortgage Group Bottom Line

Buying a home can be an exciting experience – but first you need to make sure that you are prepared financially by having good credit history and cashflow situation plus enough savings set aside for closing costs and fees associated with the purchase of the home. By following these three Martini Mortgage Group steps – preparing your credit, cashflow and savings -you will be well on your way towards becoming a homeowner in Raleigh!

If you have questions about buying a home or about securing the proper mortgage, let’s connect so you have expert advice on your side.

Kevin Martini

Kevin Martini | NMLS 143962 | Certified Mortgage Advisor | Martini Mortgage Group at Gold Star Mortgage Financial Group, Corporation | NMLS # 3446 | 507 N Blount St, Raleigh, NC 27604 | (919) 238-4934 | www.MartiniMortgageGroup.com | Kevin@MartiniMortgageGroup.com | Equal Housing Lender

Logan Martini

Logan Martini | NMLS 1591485 | Senior Mortgage Strategist | Martini Mortgage Group at Gold Star Mortgage Financial Group, Corporation | NMLS # 3446 | 507 N Blount St, Raleigh, NC 27604 | (919) 238-4934 | www.MartiniMortgageGroup.com | Logan@MartiniMortgageGroup.com | Equal Housing Lender