How Buyers and Sellers benefit from buydowns in Raleigh

A unique way that more sellers can meet more homebuyers and more homebuyers can become homeowners is with Seller-Paid Buydowns.

Kevin Martini, Certified Mortgage Advisor with Martini Mortgage Group

WHAT IS A ‘SELLER-PAID BUYDOWN’?

A ‘Seller-Paid Buydown’ is where where the seller pays a fee at the closing to reduce the interest rate on the buyer’s mortgage temporarily. This results in temporarily lowering the buyer’s monthly payment and making the home more affordable for a homebuyer today.

WHAT TYPE OF ‘SELLER-PAID BUYDOWN’ ARE AVAILABLE TODAY WITH THE MARTINI MORTGAGE GROUP?

There are three ‘Seller-Paid Buydown’ strategies offered by the Martini Mortgage Group:

1-0 Buydown…seller pays a fee at closing (the fee must be within the Interested Parties Contribution based on the loan the homebuyer is securing) to reduce the interest rate on the homebuyer’s mortgage by 1% in year 1.

2-1 Buydown…seller pays a fee at closing (the fee must be within the Interested Parties Contribution based on the loan the homebuyer is securing) reduce the interest rate on the buyer’s mortgage by 2% in year 1 and 1% in year 2.

3-2-1 Buydown…seller pays a fee at closing (the fee must be within the Interested Parties Contribution based on the loan the homebuyer is securing) reduce the interest rate on the buyer’s mortgage by 3% in year 1, 2% in year 2 and 1% in year 3.

BENEFIT OF BUYDOWN FOR A HOMEBUYER?

A buydown reduces the buyer’s interest rate and monthly payment during the first few year(s) of homeownership, making the home more affordable for homebuyers. It has a much greater impact on the homebuyer’s monthly payment than reducing the list price of the home.

BENEFIT OF BUYDOWN FOR A HOME SELLER?

A buydown could be a great negotiating tool because a greater percentage of homes listed for sale in today’s market are seeing price reductions. Not only does a buydown makes a home more affordable to a wider range of buyers who may have otherwise been priced out of the market, it also tends to cost less than a price reduction.

A seller offering to pay for a buydown could give provide a competitive advantage vs. other homes listed for sale in today’s changing market. This is because interest rates have gone up significantly this year, creating an affordability crisis for many potential buyers. As an added benefit, a buydown could also save a seller the aggravation and financial loss of having to significantly reduce your list price in order to compete with other homes that may be listed for a lower price.

In today’s market both seller and buyers need to evaluate the best approach. The best approach for a homebuyer may be with a buydown versus a price reduction and for a seller, the best approach may be to offer a buydown instead of a price reduction.

Logan Martini, Senior Mortgage Strategist with Martini Mortgage Group

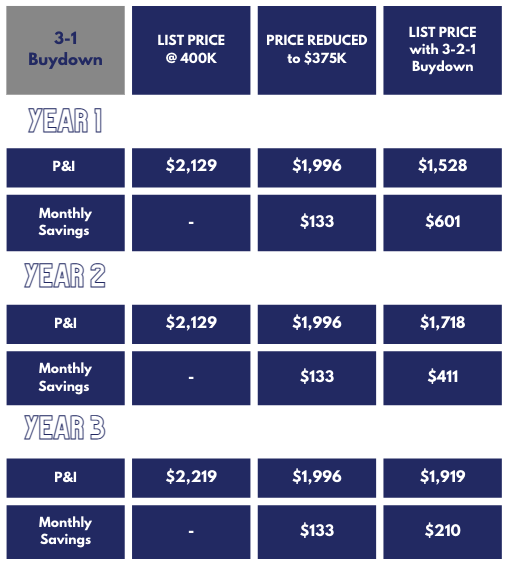

The following examples of Seller-Paid 1-1 Buydown, Seller-Paid 2-1 Buydown, 3-2-1 Seller-Paid Buydown are for illustration ONLY…assuming a sales price of $400,000 with a Borrower putting 20% down and securing a 30-year fixed mortgage with a rate of 7%. Comparing the sales price to a $25,000 price reduction to a Seller-Paid Buydown.

1-0 Buydown a.k.a. ‘Seller-Paid 1-0 Buydown’

2-1 Buydown a.k.a. ‘Seller-Paid 2-1 Buydown’

3-2-1 Buydown a.k.a. ‘Seller-Paid 3-2-1 Buydown’

Is a Seller-Paid Buydown the proper strategy for you?

I don’t know however I do know that there is never a substitute for researching your options with a Martini at the Martini Mortgage Group. For a FREE and confidential conversation, simply dial (919) 238-4934.

Logan Martini

NMLS 1591485 | Senior Mortgage Strategist

Martini Mortgage Group at Gold Star Mortgage Financial Group, Corporation | NMLS # 3446 | 507 N Blount St, Raleigh, NC 27604

Logan@MartiniMortgageGroup.com

Kevin Martini

NMLS 143962 | Certified Mortgage Advisor

Martini Mortgage Group at Gold Star Mortgage Financial Group, Corporation | NMLS # 3446 | 507 N Blount St, Raleigh, NC 27604

Kevin@MartiniMortgageGroup.com