In the ever-evolving world of real estate transactions, it is crucial for home sellers to possess a profound comprehension of the implications of capital gains tax. The sale of a home is a significant financial decision, and being well-informed about the tax aspects can enable you to make educated choices and maximize your financial gains. In this comprehensive guide, we will explore the intricacies of capital gains tax, providing valuable insights to navigate this crucial aspect of selling your home.

What is Capital Gains Tax?

Capital gains tax refers to a tax levied on the profit earned from the sale of an asset, including real estate properties. When you sell your home at a higher price than the original purchase cost, the difference is considered a capital gain. This gain is subject to taxation by the government. Understanding how this tax is calculated is essential to ensure compliance with the law and optimize your financial gains.

Determining Your Capital Gain

To ascertain your capital gain, you must calculate the disparity between the sale price of the property and its adjusted cost basis. The adjusted cost basis refers to the original purchase price of the property, adjusted for various factors such as improvements, depreciation, and transaction costs. Maintaining meticulous records of these expenses is crucial for accurately calculating your capital gain and reducing your tax liability.

Types of Capital Gains

There are two types of capital gains: short-term capital gains and long-term capital gains. The categorization depends on the duration you held the property before selling it.

Short-term Capital Gains

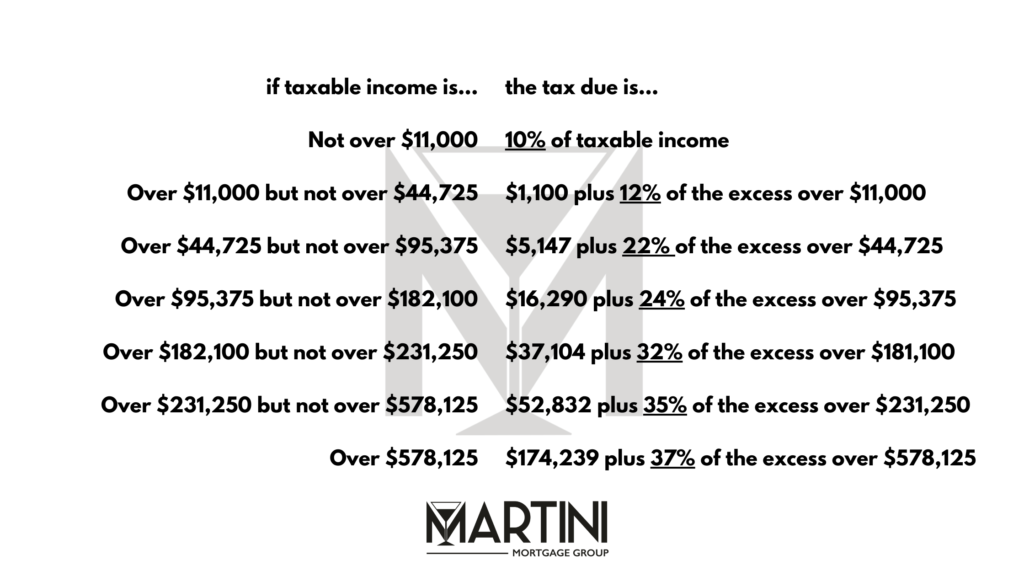

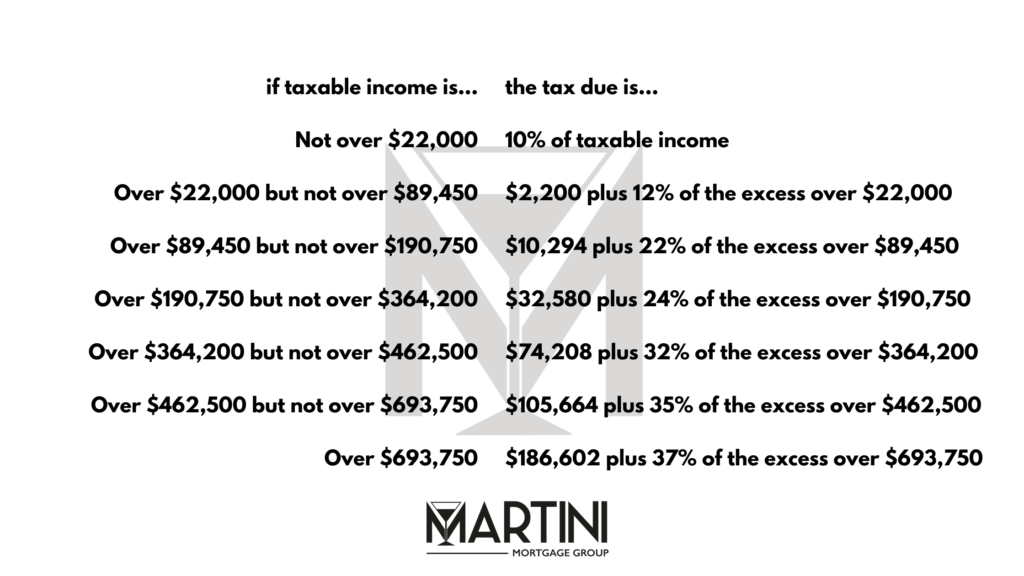

If you held the property for one year or less before selling, the resulting capital gain is considered short-term. Short-term capital gains are typically taxed at your regular income tax rate, which can be significantly higher than long-term capital gains tax rates.

Long-term Capital Gains

If you held the property for more than one year before selling, the capital gain is classified as long-term. Long-term capital gains enjoy preferential tax rates, which are generally lower than regular income tax rates. The exact tax rates for long-term capital gains vary based on your income level and the applicable tax laws.

Exemptions and Deductions

Although capital gains tax is applicable to most real estate transactions, there are certain exemptions and deductions that can help reduce your tax liability.

Primary Residence Exemption (a.k.a. Section 121 exclusion)

If the property you are selling is your primary residence and you meet specific criteria, you may qualify for a primary residence exemption. This exemption allows you to exclude a portion of your capital gain from taxation. According to U.S. tax laws, you may be able to exclude up to $250,000 of your capital gains from tax if you are single, or up to $500,000 if you are married and filing jointly. This exclusion is available if you have lived in and owned the home for at least two of the last five years before selling. It is important to refer to IRS Publication 523 and IRS Publication 544 for more information and to consult with a tax professional to understand the eligibility criteria, as specific rules and limitations apply.

Taxable Gain Exclusion

Even if you have a taxable gain on the sale of your home, you might still be able to exclude a portion of it if you sold the house due to work, health reasons, or “an unforeseeable event,” as defined by the IRS. For specific details and eligibility requirements, you can refer to IRS Publication 523.

Capital Improvements

The cost of capital improvements made to your property, such as renovations or additions, can be added to your adjusted cost basis. By increasing the adjusted cost basis, you effectively reduce your capital gain and subsequently lower your tax liability.

Strategies for Minimizing Capital Gains Tax

While it is not possible to completely avoid capital gains tax, there are several strategies you can employ to minimize its impact on your financial outcome.

Tax Loss Harvesting

If you have other investments that have incurred capital losses, strategically selling those assets can offset your capital gains. This technique, known as tax loss harvesting, helps reduce your overall tax liability. To understand the eligibility criteria and specific rules and limitations, it is crucial to consult with a tax professional.

1031 Exchange (for investment properties only)

Under Section 1031 of the Internal Revenue Code, you can defer paying capital gains tax by reinvesting the proceeds from the sale of one property into the purchase of another similar property. This strategy, commonly known as a 1031 exchange or like-kind exchange, allows you to postpone your capital gains tax liability and potentially expand your real estate portfolio.

Raleigh Mortgage Broker Logan Martini Bottom Line

Understanding capital gains tax is crucial for home sellers to navigate the intricacies of real estate transactions successfully. By comprehending the tax implications and employing strategic techniques to minimize your tax liability, you can optimize your financial outcome. Remember to consult professionals who can provide expert advice tailored to your specific situation since this article serves for informational purposes only and should not be considered legal, tax, or financial advice.

Given the complexities of capital gains tax and its implications, it is advisable to seek professional guidance from a qualified tax advisor. They can provide personalized advice based on your unique circumstances, ensuring compliance with tax regulations and helping you make the most informed decisions.

Logan Martini | NMLS 1591485 | Senior Mortgage Strategist | Martini Mortgage Group at Gold Star Mortgage Financial Group, Corporation | NMLS # 3446 | 507 N Blount St, Raleigh, NC 27604 | (919) 238-4934 | www.MartiniMortgageGroup.com | Logan@MartiniMortgageGroup.com | Equal Housing Lender