If you’ve been wondering whether it’s better to rent or buy a home, you’re not alone. The past year has brought uncertainty to the real estate market, leaving many unsure about their next move. But here’s the exciting part: the market is transitioning, and this shift presents unique opportunities for those ready to embrace homeownership.

Owning a home is more than having a place to call your own—it’s a financial strategy. In episode 198 of the Martini Mortgage Podcast called “Owning Your Roof vs Renting” Certified Mortgage Advisor and Raleigh Mortgage Broker Kevin Martini explores why this season is ideal for buying a home and how homeownership can transform your financial future.

The Wealth Gap: Renting vs. Owning

Here’s a staggering fact: the net worth of a homeowner is 42 times greater than that of a renter. That’s $415,000 compared to just $10,000. This wealth gap isn’t just significant—it’s growing. If you’re renting, every dollar you spend contributes to your landlord’s financial future, not yours.

Owning your roof isn’t just about stability—it’s about building long-term wealth. As home values rise (and they almost always do), your investment grows, setting you up for financial security and freedom.

Why Homeownership Matters Right Now

There’s never been a more critical time to rethink renting. Rising rents are leaving renters vulnerable to increasing costs, while homeowners with a fixed-rate mortgage enjoy predictable housing expenses.

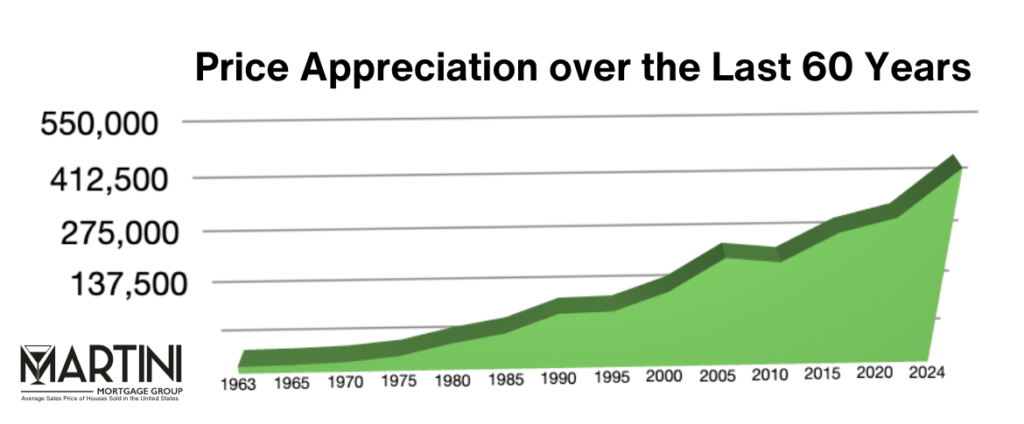

Let’s face it: renting might make sense for a season, but this is not that season. With home values increasing by over 57% in the past five years and more than tripling in the last 30, waiting on the sidelines could mean missing out on wealth-building opportunities.

Over the past 5 years, the average home’s value has skyrocketed by more than 57%. Now, take a step back and look at the bigger picture—over the last 30 years, home values have more than tripled!

Certified Mortgage Advisor and Raleigh Mortgage Broker Kevin Martini

Debunking Raleigh Homeownership Myths

Many believe they need perfect credit or a massive down payment to buy a home. Here’s the truth: you don’t. Most people overestimate the barriers to homeownership, relying on misinformation instead of facts.

At Martini Mortgage Group, we’re here to help you navigate the process with accurate information and a strategy tailored to your unique situation.

Why Waiting Could Cost You

You might be thinking, “Why not wait until mortgage rates go down?” While it’s a fair question, the reality is that when rates drop, demand surges. Historically, a 1% decrease in mortgage rates introduces 5 million new buyers into the market, creating fierce competition and driving home prices higher.

By acting now, you can lock in your costs and refinance later when rates improve. Waiting could cost you far more in rising home prices than you save on interest.

Owning Your Roof vs. Renting It: Why Now is the Time to Buy

If you’ve been wondering whether it’s better to rent or buy a home, you’re not alone. The past year has brought uncertainty to the real estate market, leaving many unsure about their next move. But here’s the exciting part: the market is transitioning, and this shift presents unique opportunities for those ready to embrace homeownership.

Owning a home is more than having a place to call your own—it’s a financial strategy. In this blog, we’ll explore why this season is ideal for buying a home and how homeownership can transform your financial future.

The Wealth Gap: Renting vs. Owning

Here’s a staggering fact: the net worth of a homeowner is 42 times greater than that of a renter. That’s $415,000 compared to just $10,000. This wealth gap isn’t just significant—it’s growing. If you’re renting, every dollar you spend contributes to your landlord’s financial future, not yours.

Owning your roof isn’t just about stability—it’s about building long-term wealth. As home values rise (and they almost always do), your investment grows, setting you up for financial security and freedom.

Why Homeownership Matters Right Now

There’s never been a more critical time to rethink renting. Rising rents are leaving renters vulnerable to increasing costs, while homeowners with a fixed-rate mortgage enjoy predictable housing expenses.

Let’s face it: renting might make sense for a season, but this is not that season. With home values increasing by over 57% in the past five years and more than tripling in the last 30, waiting on the sidelines could mean missing out on wealth-building opportunities.

Debunking Homeownership Myths

Many believe they need perfect credit or a massive down payment to buy a home. Here’s the truth: you don’t. Most people overestimate the barriers to homeownership, relying on misinformation instead of facts.

At Martini Mortgage Group, we’re here to help you navigate the process with accurate information and a strategy tailored to your unique situation.

Why Waiting Could Cost You

You might be thinking, “Why not wait until mortgage rates go down?” While it’s a fair question, the reality is that when rates drop, demand surges. Historically, a 1% decrease in mortgage rates introduces 5 million new buyers into the market, creating fierce competition and driving home prices higher.

By acting now, you can lock in your costs and refinance later when rates improve. Waiting could cost you far more in rising home prices than you save on interest.

Create Your Homeownership Strategy

Buying a home is one of the most important financial decisions you’ll ever make. But not every opportunity will be the right fit for you. That’s why it’s crucial to approach homeownership with a clear plan based on facts, not fear.

At Martini Mortgage Group, we offer complimentary, no-judgment consultations to help you determine whether now is the right time for you to buy. Together, we’ll craft a strategy that aligns with your goals, ensuring you’re positioned for success.

Why the Martini Mortgage Group?

With decades of experience in financial services and the mortgage industry, Kevin Martini and the Martini Mortgage Group are trusted partners for families across Raleigh and the Southeast. As a Raleigh Mortgage Broker and Certified Mortgage Advisor, Kevin’s mission is to empower clients with the knowledge and tools they need to achieve homeownership.

Whether you’re buying your first home or considering a refinance, the Martini Mortgage Group is here to help you navigate the journey with confidence.

Let’s Make Your Homeownership Dreams a Reality

This moment in the real estate market could be a once-in-a-lifetime opportunity to take control of your financial future. If you’re ready to explore your options, reach out today for a personalized consultation.

Call Kevin Martini at (919) 238-4934 for more insights on why owning your roof is the smartest move you can make this year.