Raleigh mortgage broker Logan Martini with the Martini Mortgage Group offers a bank statement mortgage program to help self-employed borrowers who are in need of an alternate method to show the true cash flow of their business to qualify for a home loan.

It is my opinion that self-employed borrowers are simply not properly represented by mortgage lenders and mortgage brokers in the market place today. Myself and the Martini Mortgage Group may be based in Raleigh but we help credit worthy self-employed borrowers all over North Carolina and in many state in the U.S. who would other wise not qualify for a home loan the traditional way.

Senior Mortgage Strategist, Logan Martini

Martini Mortgage Group Bank Statement Mortgage Program

With the Martini Mortgage Group Bank Statement Mortgage Program a borrower does not need to have 100% ownership in the company to qualify. There are 2 Bank Statement Mortgage options:

a) a 12-month option using business and/or personal bank statements or

b) 24-month option using business and/or personal bank statements.

For either option (e.g. 12-month or 24-month), 2-years of self-employment history is required.

The Bank Statement Mortgage Program can be used for a purchase of a home or a refinance of a current mortgage. The refinance can either be a rate-term refinance or cash-out refinance. The credit score does not need to be perfect either, borrowers with credit scores starting at 600 are eligible. The loan-to-value (LTV) can be up to 90% and the Martini Mortgage Group Bank Statement Program does not carry mortgage Insurance. Oh by the way, the minimum loan amount is $150,000 and the maximum is up to $3,000,000.

To learn more about the Bank Statement Mortgage Program offered by Raleigh mortgage broker Logan Martini, simple call (919) 238-4934.

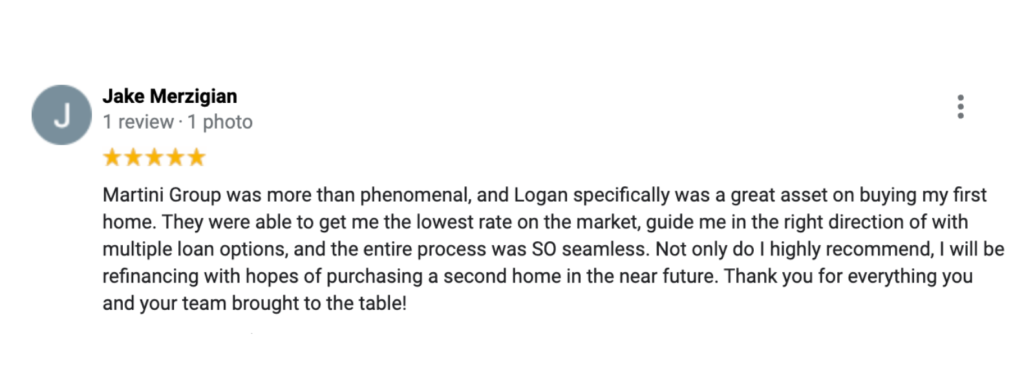

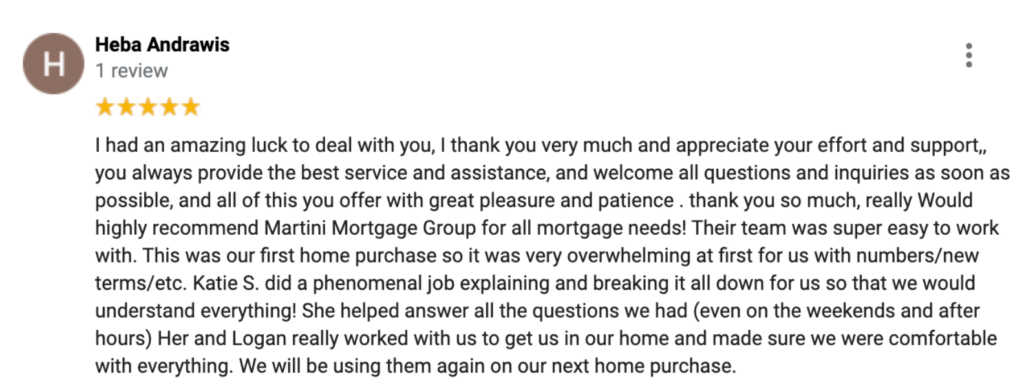

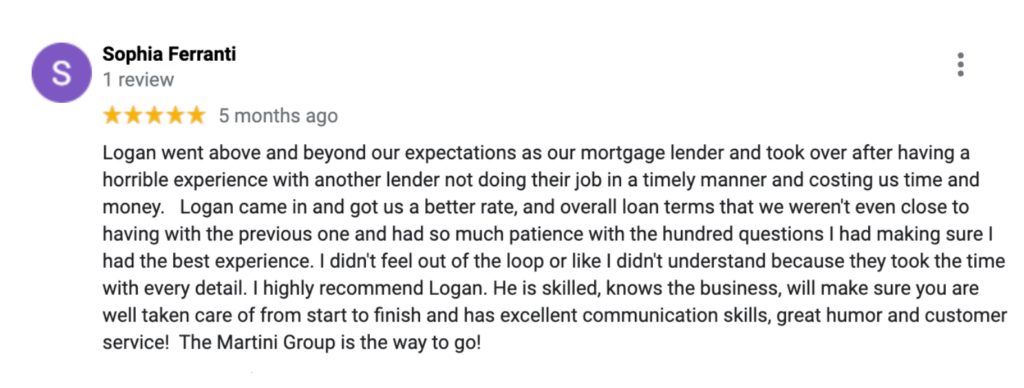

What people say about working with Raleigh Mortgage Broker Logan Martini