Many people are curious what will happen to home values over the next few years. Some renters think they need to keep renting and some homeowners think they should stay stay in the house they now own even though it does not meet their current or future needs because of fear of a real estate shift. Oh by the way, shift is a euphemism for real estate bubble. SPOILER ALERT – there we are not in a a real estate bubble zone, we are in a real estate opportunity zone!

In this special episode of the Martini Mortgage Podcast called, if not now, it could really cost you; Certified Mortgage Advisor Kevin Martini breaks down the economics based on what a dynamic group of 100+ economists, housing market analyst and investment strategists are predicting for the next 5-years.

Martini Mortgage Podcast | Episode 140 | If not now, it could really cost you!

Right now, that means today we are living in the good old days of real estate. What do I mean by that? Simply put, if you fast forward 5-years or 15-years and you look at today, you will say one of two things…you will either say, I am so thankful that I purchased real estate in 2022 or you will say I wish I had purchased real estate in 2022, it truly was the good old days of real estate back then.

Kevin Martini – Certified Mortgage Advisor & Raleigh Mortgage Broker

Home Price Expectation Survey

Martini Mortgage Podcast Transcript of Episode 140

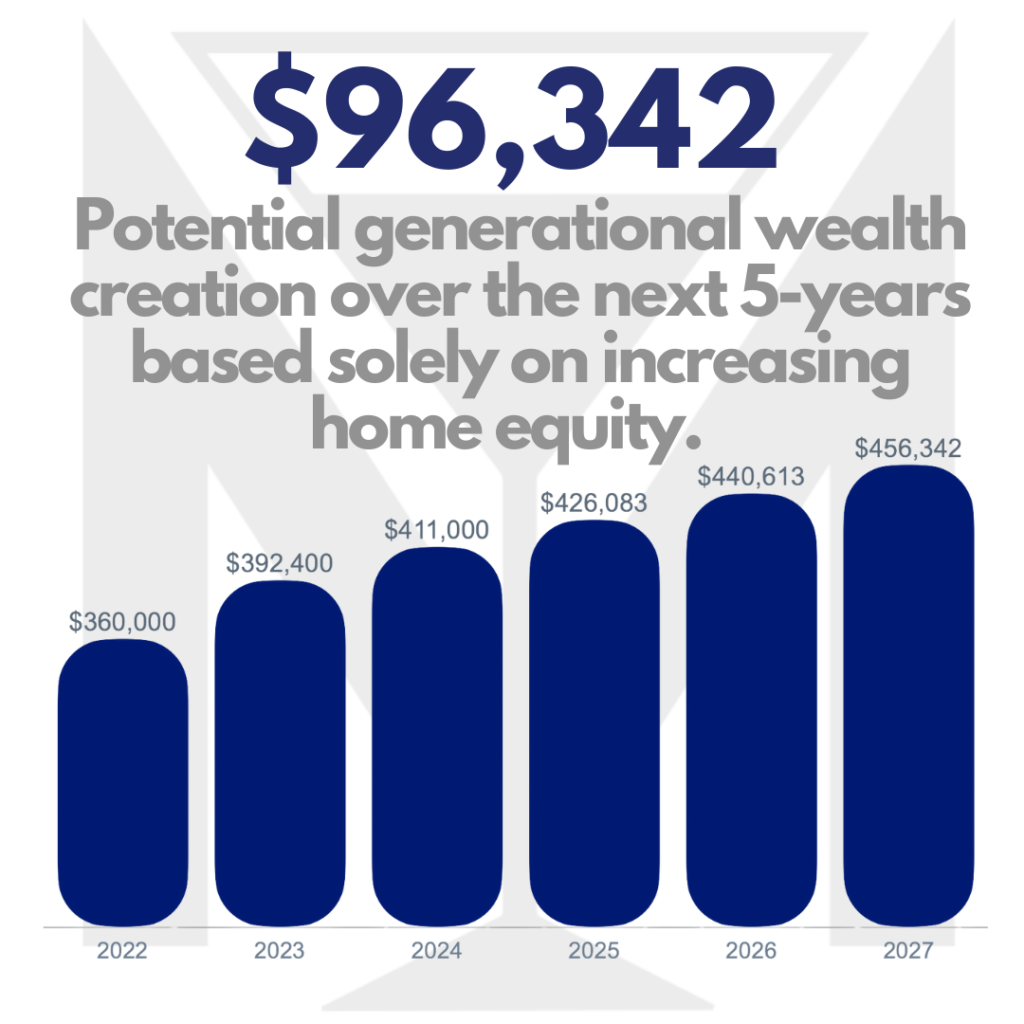

If not now, it could really cost you! When I say now, I mean right now and when I say it could cost you, I mean it could cost you tens of thousands of dollars. In fact, according to the Home Price Expectation Survey it could cost you $32,400 in 2022 and by the end of 2027, it could cost you $96,343 in appreciation alone. Then there are rising mortgage rates. Let me share this hashtag Kevin Martini Live nugget about mortgage rates. When mortgage rates rise by just one-percent than your buying power is reduced by over 10%.

Welcome to episode 140 of the Martini Mortgage Podcast, my name is Kevin Martini and I am a Certified Mortgage Advisor with the Martini Mortgage Group which is located in Raleigh, North Carolina however myself along with my very talented crew help families in all 100 counties of North Carolina and pretty much in ever state in the U.S. too. I am calling this special episode of the Martini Mortgage Podcast; If not now, it could really cost you!

Right now, that means today we are living in the good old days of real estate. What do I mean by that? Simply put, if you fast forward 5-years or 15-years and you look at today, you will say one of two things…you will either say, I am so thankful that I purchased real estate in 2022 or you will say I wish I had purchased real estate in 2022, it truly was the good old days of real estate back then.

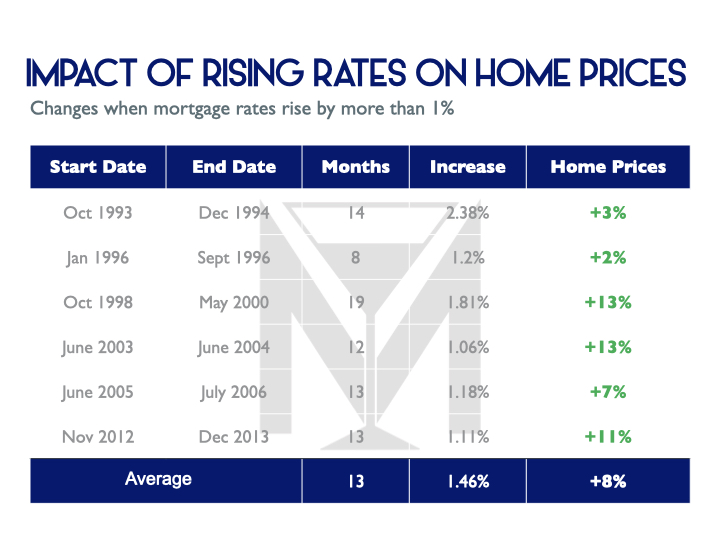

Let us talk about where real estate is going in light of higher mortgage rates appearing in 2022. Wait! Yes, mortgage rates are higher today than they have been in the last couple of years however from a historical standard, they are historically low. Bold statement, not really — check this out. If you looked at historical 30-year fixed mortgage rates since 1971 the average rate is pretty darn close to 8 percent. Again, from a historical standard, mortgage rates are cheap but they will not be forever.

Now to me, it is not what one person opinion is that matters. Opinions are like belly buttons, everyone has one. I like to look at a sampling of what many experts think when I look at the future of real estate values and the Home Price Expectation Survey that is performed by Pulesnomics is in my opinion the most accurate predictor future of home value. You see the Home Price Expectation Survey is not just what one person thinks, it is a survey of 100+ real estate market experts, economists and investment strategists.

The forecast in the most recent Home Price Expectation Survey highlights that home prices will continue to appreciate over the next 5-years. In 2022, the see a deceleration of appreciation and in 2023 through a stabilization of home values to more traditional levels.

I want to be crystal clear, deceleration of home values does not mean that home values are going to depreciate. Nor does deceleration of home values means that there is a real estate bubble that is going to burst like they did 15-years ago during the great recession. Also while I am setting the official record straight, let me properly communicate, for the people in the back, recession does not mean housing bubble nor does recession means a depreciation of home values.

Let me share a Kevin Martini story with you. Let us assume you are on Interstate 40 leaving Raleigh and going East towards Wilmington. The speed limit is 65 however you are going 85 miles per hour and in the distance you see a police car…you decelerate and take your speed to the posted speed limit of 65. You pass the police car and there are no blue lights flashing in your rearview mirror.

Sure you are now going 20 miles per hour slower however your are still going the speed limit. It is my opinion that this is what real estate is going to do int he coming years — it is going to decelerate not depreciate. Yes the two words sound alike but they have materially different meaning.

The Home Price Expectation Survey is predicting a a 9% increase in home values in 2022. According the Federal Housing Finance Agency the year of year appreciation in 2021 was 18.8%. The S&P Case-Shiller was up 18.6% so yes, a 9% predication is deceleration but it is still above the historical average and that means we are still speeding.

Don’t believe me that we will still be speeding in 2022? Let me share that the Martini Mortgage Group is located in Raleigh, North Carolina. Raleigh, North Carolina is located in Wake County and the 63-year average yearly home appreciation rate 3.41% for Wake County, North Carolina.

The Home Price Expectation Survey says that in Raleigh, North Carolina and specifically Wake County, North Carolina we will keep speeding in 2023 with a forecasted home appreciation rate of 4.74% and in 2024 the appreciation rates hold be 3.67% and in 2025, we will be at the current 63-year average in Wake County with 3.41% and then in 2026, 3.57% appreciation.

Holy cow that was a lot of numbers, what does it all mean? For illustration, let us assume that you purchased a $360,000 home in January 2022. According to the predications in the Home Price Expectation Survey by the end of 2023 that home will be worth 392,400 and in 2024 it will be worth $411,000 well let me fast forward to the end of 2026, that home would be worth $456,343.

The very distinguished panel that is survey for the Home Price Expectation Survey is stating that you could have a potential growth in household wealth over the next 5-year of $96,343 solely on increased home equity.

I said it earlier during the episode of the Martini Mortgage Podcast, we are living in the good old days of real estate and if not now, it could really cost you!

In closing, there is nothing wrong with renting and there is a time to rent however, in my opinion, that time is not now. I want to be clear, renting may be the right thing for you and your family but I truly believe, with an open heart, you need confirmation that homeownership is not right for you and your family. Right now is the time to explore your homeownership option based on facts not based on what you heard at a barbecue a couple of years ago.

If you want or need mortgage help to explore you homeownership options as a first time home buyer or as a repeat home buyer … know that we are here to help, just give us a jingle at 919.238.4934.

Again, my name is Kevin Martini and I am a Certified Mortgage Advisor with the Martini Mortgage Group which is located in Raleigh, North Carolina however I help families all over the U.S.. If you are buying a home and need a home loan, know that I provide trusted advice with a frictionless process that offers great rates and certainty to you and your family. Real estate transactions need to always close on-time and need to be stress-free and should be a world-class experience for everyone involved.

Stay safe out there and wishing you peace and blessings.

Now it is time for the disclaimer:

This material has been prepared for marketing purposes only. This is not a loan commitment or guarantee of any kind. Loan approval and rate are dependent upon borrower credit, collateral, financial history, and program availability at time of origination. Rates and terms are subject to change without notice. The Martini Mortgage Group at PCL Financial is a division of Celebrity Home Loans, NMLS # 227765 with a Branch address of 507 N Blount St Raleigh, North Carolina 27604. You can contract Certified Mortgage Advisor and Producing Branch Manager, Kevin Martini NMLS# 143962 by calling the Branch and that number is 919.238.4934. For a full list and more licensing information please visit: www.NMLSConsumerAccess.org or by visiting www.MartiniMortgageGroup.com – Equal Housing Lender