What is going on in real estate and home loan rates is the name of a new monthly series being produced by the Martini Mortgage Group for the Martini Mortgage Podcast. Episode 161 is the inaugural issue.

I truly believe episode 161 is one of the most important, if not the most important, that Logan and I have produced to date.

Kevin Martini, Certified Mortgage Broker

Video Edition of Martini Mortgage Podcast episode 161 called: What is going on in Real Estate and Home Loan Rates (October 2022 Edition)

Audio Edition of Martini Mortgage Podcast episode 161 called: What is going on in Real Estate and Home Loan Rates (October 2022 Edition)

Transcript of Martini Mortgage Podcast episode 161 called: What is going on in Real Estate and Home Loan Rates (October 2022 Edition)

1

00:00:00,620 –> 00:00:04,726

[kevin_martini]: there’s a lot of scary headlines out

there right now which are highlight in the

2

00:00:04,807 –> 00:00:09,895

[kevin_martini]: sudden rise of mortgage rates the increase

in house inventory people are now talking about

3

00:00:10,035 –> 00:00:15,012

[kevin_martini]: the future of real estate and then

you have inflation two this is a new

4

00:00:15,152 –> 00:00:19,645

[kevin_martini]: special video and audio edition of the

new monthly series from the markin mortgage group

5

00:00:19,725 –> 00:00:26,039

[kevin_martini]: that we are calling what is going

on now before i start mixing it up

6

00:00:26,921 –> 00:00:33,153

[kevin_martini]: i need to make those legal folks

happy so the primary purpose of this podcast

7

00:00:33,213 –> 00:00:40,165

[kevin_martini]: series is to inform entertain and educate

the information opinions and recommendations presented in this

8

00:00:40,285 –> 00:00:46,455

[kevin_martini]: podcast series do not constitute legal or

their professional advice opinions or endorsements of any

9

00:00:46,615 –> 00:00:53,226

[kevin_martini]: kind welcome to the martini mortgage podcast

episode one hundred and sixty one i’m calling

10

00:00:53,287 –> 00:00:58,973

[kevin_martini]: it what is going on in october

twenty twenty two inaugural issue my name is

11

00:00:59,073 –> 00:01:04,983

[kevin_martini]: kevin martini and i am a certified

mortgage advisor and producing branch manager and i’m

12

00:01:05,103 –> 00:01:08,629

[kevin_martini]: less one four three nine six two

with the martini mortgage group back gold star

13

00:01:08,870 –> 00:01:16,377

[kevin_martini]: gage financial group corporation and les three

four four six equal house seen lender with

14

00:01:16,477 –> 00:01:21,811

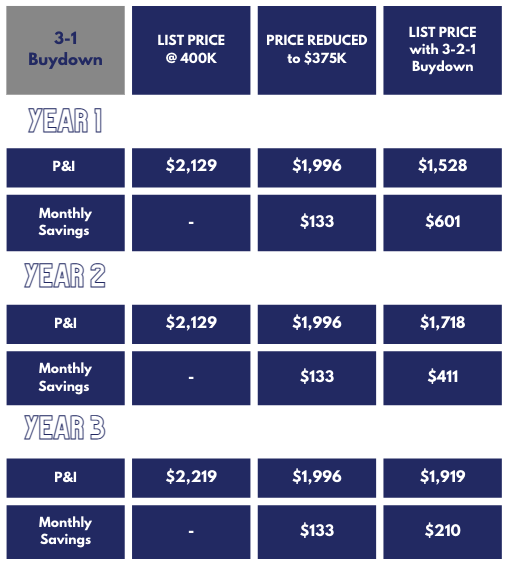

[kevin_martini]: all that said let’s dive into the

news on friday october seventh the bureau of

15

00:01:21,931 –> 00:01:29,558

[kevin_martini]: labor statistics reported that two hundred and

sixty three thousand jobs were created in september

16

00:01:29,658 –> 00:01:36,473

[kevin_martini]: twenty twenty two and this was above

the expectations the unemployment rate decrease from three

17

00:01:36,574 –> 00:01:42,724

[kevin_martini]: point seven to three point five per

cent to the data from these reports spook

18

00:01:42,864 –> 00:01:48,934

[kevin_martini]: the markets because it provides an unofficial

signal that the fad will continue on its

19

00:01:49,115 –> 00:01:55,306

[kevin_martini]: tightening journey and it is likely to

be very aggressive to get inflation under control

20

00:01:55,427 –> 00:02:02,926

[kevin_martini]: moving forward let me be clear the

fan needs tightening because they need to reduce

21

00:02:02,966 –> 00:02:10,218

[kevin_martini]: demand in the market place and this

reduced demand should be the thing that teams

22

00:02:10,278 –> 00:02:15,824

[kevin_martini]: the beast and that beast is inflation

it is my opinion the fed will raise

23

00:02:15,984 –> 00:02:22,195

[kevin_martini]: rates in the november and december meetings

i also believe the fed fung rate could

24

00:02:22,255 –> 00:02:30,295

[kevin_martini]: be increased by one and a half

point it is an undisputable fact we have

25

00:02:30,396 –> 00:02:35,865

[kevin_martini]: not seen inflation at this level for

decades and the fens actions to be transparent

26

00:02:35,945 –> 00:02:43,097

[kevin_martini]: have helped but they’ve helped incrementally but

inflation is still persistent and high this is

27

00:02:43,257 –> 00:02:49,668

[kevin_martini]: critical because inflation is the nemesis or

the arch enemy to mortgage rates you see

28

00:02:50,820 –> 00:02:55,934

[kevin_martini]: mortgage rates are not controlled by the

federal reserve nor do mortgage rates come from

29

00:02:56,015 –> 00:03:02,653

[kevin_martini]: the stock market mortgage rates live in

the bond market inflating a road the return

30

00:03:03,075 –> 00:03:08,185

[kevin_martini]: of a bond just because there is

inflation it does not mean the markets will

31

00:03:08,285 –> 00:03:14,515

[kevin_martini]: stop in the simplest of examples market

makers will offer a higher yield to a

32

00:03:14,616 –> 00:03:22,748

[kevin_martini]: mortgage bond investor when more gage bond

yield is increased that means mortgage rates will

33

00:03:22,948 –> 00:03:28,823

[kevin_martini]: go higher now i feel that the

feds actions will get inflation under control in

34

00:03:28,883 –> 00:03:34,468

[kevin_martini]: the first quarter of twenty twenty three

it’s critical that i share this based on

35

00:03:34,628 –> 00:03:40,517

[kevin_martini]: history the fact has always been late

to the party and they stayed too long

36

00:03:40,597 –> 00:03:45,305

[kevin_martini]: to the party they were clearly too

late to this party because they thought inflation

37

00:03:45,405 –> 00:03:54,367

[kevin_martini]: was transiatory not sticky the developing story

is what will they do when inflationary pressures

38

00:03:54,728 –> 00:04:02,437

[kevin_martini]: are east stay tuned i think they

will stay after the party is over and

39

00:04:02,517 –> 00:04:10,841

[kevin_martini]: then they will promoting growth rapid massive

growth and this growth will provide a sharp

40

00:04:11,242 –> 00:04:17,019

[kevin_martini]: drop in mortgage rates by the way

that’s just not me fan may has said

41

00:04:17,080 –> 00:04:24,192

[kevin_martini]: that too let’s talk about mortgage rates

for a hot second for some the current

42

00:04:24,273 –> 00:04:29,682

[kevin_martini]: rate environment was not possible however for

a long term fans of the martini mortgage

43

00:04:29,742 –> 00:04:35,176

[kevin_martini]: podcast they were advised that this was

likely to happen and for those new fans

44

00:04:35,297 –> 00:04:41,786

[kevin_martini]: let me be clear it is probable

that mortgage rates will get worse before they

45

00:04:41,846 –> 00:04:48,752

[kevin_martini]: get better it is not unthinkable that

mortgage rates could start with an eight sooner

46

00:04:49,154 –> 00:04:56,289

[kevin_martini]: than later there are advanced strategies offered

by myself and fellow morgan strategist logan martine

47

00:04:56,349 –> 00:05:02,279

[kevin_martini]: to help today and in the future

too if home ownership is right for you

48

00:05:02,459 –> 00:05:07,227

[kevin_martini]: as first time home buyer or as

a repeat home buyer one of the many

49

00:05:07,488 –> 00:05:14,900

[kevin_martini]: options is the martini mortgage group no

contract lock program with a free flow down

50

00:05:15,561 –> 00:05:22,993

[kevin_martini]: up to ninety days this is a

very simple program but it is very powerful

51

00:05:23,775 –> 00:05:29,003

[kevin_martini]: here’s how it works a future home

buyer ken lock their mortgage rate at to

52

00:05:29,084 –> 00:05:35,334

[kevin_martini]: day’s price and that price can be

protected for up to ninety days in the

53

00:05:35,414 –> 00:05:39,782

[kevin_martini]: event there’s an improvement in the rate

when the future home buyer goes under contract

54

00:05:40,183 –> 00:05:44,815

[kevin_martini]: for their new home they will have

the option to float the right down to

55

00:05:44,856 –> 00:05:53,546

[kevin_martini]: the improved right how cool is that

this unique no contract lock program can be

56

00:05:53,586 –> 00:05:59,275

[kevin_martini]: combined with a seller paid by down

program offered by the martini mortgage group for

57

00:05:59,335 –> 00:06:04,504

[kevin_martini]: more information about the seller paid by

down check out episode one five nine of

58

00:06:04,544 –> 00:06:12,057

[kevin_martini]: the martini mortgage podcast since it explains

it in great detail the benefits of a

59

00:06:12,157 –> 00:06:18,903

[kevin_martini]: seller paid by down just give you

a glimpse if that’s okay real belief fly

60

00:06:18,983 –> 00:06:23,990

[kevin_martini]: there are three types of by downs

there’s a one one by down there’s a

61

00:06:24,371 –> 00:06:30,040

[kevin_martini]: two one by down and there’s a

three to one by down for illustration only

62

00:06:30,161 –> 00:06:35,670

[kevin_martini]: let’s assume your rate you lock with

our no contract lock program at six per

63

00:06:35,730 –> 00:06:42,560

[kevin_martini]: cent and let us assume you negotiate

or two one seller paid buy down this

64

00:06:42,700 –> 00:06:47,027

[kevin_martini]: would mean in the first year your

rate would be four per cent and in

65

00:06:47,068 –> 00:06:50,914

[kevin_martini]: the second year your rate would be

five per cent and then it would go

66

00:06:51,114 –> 00:06:57,733

[kevin_martini]: to six for your three through thirty

seller paid buy downs are a win win

67

00:06:58,396 –> 00:07:06,462

[kevin_martini]: since this program benefits both the seller

and the buyer too it’s not just me

68

00:07:06,783 –> 00:07:16,610

[kevin_martini]: but it is many experts believe that

the mortgage rates will significantly improve towards the

69

00:07:16,731 –> 00:07:22,039

[kevin_martini]: end of twenty twenty three to the

beginning of twenty twenty four the experts that

70

00:07:22,140 –> 00:07:26,447

[kevin_martini]: our bullets she that could be as

soon as the second quarter of twenty twenty

71

00:07:26,487 –> 00:07:31,242

[kevin_martini]: three to be transparen i think the

bulls are being a little bit too aggressive

72

00:07:31,302 –> 00:07:36,603

[kevin_martini]: and running too fast here is the

punch line the home loan rate you get

73

00:07:36,683 –> 00:07:40,190

[kevin_martini]: today is not likely going to be

the home loan rate you will have in

74

00:07:40,230 –> 00:07:45,891

[kevin_martini]: a couple of years because when the

thed gets inflation under control again when not

75

00:07:46,071 –> 00:07:51,736

[kevin_martini]: if and while they are staying at

the party too long which they will there

76

00:07:51,876 –> 00:07:57,876

[kevin_martini]: are going to be re finance opportunities

according to fanny may as i said earlier

77

00:07:58,156 –> 00:08:04,515

[kevin_martini]: they expect rates to start with the

four sometime in twenty twenty three this is

78

00:08:04,635 –> 00:08:11,869

[kevin_martini]: why the phrase marry the house and

date the rate is being said so frequently

79

00:08:11,949 –> 00:08:20,737

[kevin_martini]: by myself my fellow mortgage strategist logan

martini and others let me break it down

80

00:08:21,770 –> 00:08:28,080

[kevin_martini]: it is very probable that mortgage rates

will increase over the next three to six

81

00:08:28,280 –> 00:08:34,497

[kevin_martini]: months to levels that millennials have never

seen and even some folks that are generation

82

00:08:34,800 –> 00:08:42,117

[kevin_martini]: exerts mortgage rates are not the only

thing going up rents are going up to

83

00:08:43,090 –> 00:08:48,900

[kevin_martini]: don’t believe me well let me share

the facts in rale north carolina from july

84

00:08:49,100 –> 00:08:54,589

[kevin_martini]: twenty twenty one to july twenty twenty

two rents for one bedroom apartment went up

85

00:08:55,250 –> 00:08:59,657

[kevin_martini]: two point one per cent and a

two bedroom apartment went up forty four point

86

00:08:59,838 –> 00:09:05,848

[kevin_martini]: eight per cent in durham the bull

city of north carolina for the same period

87

00:09:05,928 –> 00:09:11,250

[kevin_martini]: of time to every apartment went up

fifty four point two per cent you know

88

00:09:11,310 –> 00:09:17,861

[kevin_martini]: what else is going up home values

did you know that three point eight four

89

00:09:18,122 –> 00:09:24,574

[kevin_martini]: per cent is the average annual growth

in home prices from ten eighty nine to

90

00:09:24,735 –> 00:09:32,198

[kevin_martini]: two thousand nineteen check it out i

took out the eighteen point five per cent

91

00:09:32,338 –> 00:09:38,068

[kevin_martini]: of annual appreciation per year for the

last two years of this calculation because the

92

00:09:38,730 –> 00:09:46,075

[kevin_martini]: home christ growth during the presence of

the eagle pandemic was a typical so three

93

00:09:46,155 –> 00:09:52,880

[kevin_martini]: point eight four per cent is the

past what about the future it is my

94

00:09:53,001 –> 00:09:58,890

[kevin_martini]: opinion what one person says about the

future of home values is irrelevant for me

95

00:09:59,491 –> 00:10:04,239

[kevin_martini]: and for the families the martini mortgage

group serves the gold standard of future home

96

00:10:04,520 –> 00:10:10,791

[kevin_martini]: uses the home price expectation survey done

every quarter by pullsnomics and that is because

97

00:10:10,871 –> 00:10:17,091

[kevin_martini]: it’s not one person’s opinion it is

the opinion of over one hundred experts oh

98

00:10:17,191 –> 00:10:23,201

[kevin_martini]: by the way the home price expectation

survey is expecting a five year cumulative appreciation

99

00:10:23,762 –> 00:10:30,739

[kevin_martini]: of over twenty four percent closer to

twenty five actually let me get granular for

100

00:10:30,800 –> 00:10:37,347

[kevin_martini]: a hot second let me not use

the current forecast from the home price expectation

101

00:10:37,487 –> 00:10:43,959

[kevin_martini]: survey data nor the data from the

past twenty years prior to the evil pandemic

102

00:10:45,400 –> 00:10:51,792

[kevin_martini]: let me be super conservative and let

me just say three percent appreciation a year

103

00:10:52,293 –> 00:10:59,012

[kevin_martini]: for the next five years what would

this mean simply put a fifteen thousand dollar

104

00:10:59,072 –> 00:11:05,478

[kevin_martini]: down payment on a three hundred thousand

house could grow to sixty two thousand dollars

105

00:11:05,558 –> 00:11:12,033

[kevin_martini]: over five years twenty five thousand dollar

thou payment on a five hundred thousand dollar

106

00:11:12,114 –> 00:11:19,370

[kevin_martini]: house could grow to a hundred and

four thousand dollars in over five years a

107

00:11:19,590 –> 00:11:25,600

[kevin_martini]: forty five thousand dollar down payment on

a nine hundred thousand dollar home could grow

108

00:11:25,801 –> 00:11:33,723

[kevin_martini]: to a hundred and eighty eight thousand

dollars over five years not owning a home

109

00:11:34,364 –> 00:11:42,005

[kevin_martini]: could not just cost you thousands but

tens of thousands it’s in we all have

110

00:11:42,065 –> 00:11:46,902

[kevin_martini]: to have a roof over our head

some will rent it and when you rent

111

00:11:47,222 –> 00:11:52,716

[kevin_martini]: you pay a mortgage you’re not paying

your mortgage you’re just paying for your landlords

112

00:11:52,816 –> 00:11:59,365

[kevin_martini]: mortgage for them others will own that

roof and logan martini and myself help them

113

00:11:59,525 –> 00:12:05,734

[kevin_martini]: secure the proper mortgage strategy for that

roof let me say this another way for

114

00:12:05,814 –> 00:12:13,037

[kevin_martini]: the people the back the growth in

home appreciation has decelerated in twenty twenty two

115

00:12:13,398 –> 00:12:19,288

[kevin_martini]: but just because home prices have decelerated

it does not mean homes are going to

116

00:12:19,368 –> 00:12:27,025

[kevin_martini]: depreciate in the aggregate poets are going

to continue to appreciate and grant it in

117

00:12:27,245 –> 00:12:34,970

[kevin_martini]: some markets that were extra frothy we

may see a decline from their peak key

118

00:12:35,151 –> 00:12:43,426

[kevin_martini]: word is some markets right now home

buyers can still find opportunities and i believe

119

00:12:43,506 –> 00:12:52,690

[kevin_martini]: that today a home buyer has the

proper conditions to secure more buying power if

120

00:12:52,730 –> 00:12:56,817

[kevin_martini]: you’re thinking of buying a home for

the first time or as a repeat home

121

00:12:56,837 –> 00:13:02,486

[kevin_martini]: buyer simply give a mortgage strategist with

a martini mortgage group a jingle by dialing

122

00:13:02,546 –> 00:13:08,784

[kevin_martini]: nine one nine two three eight forty

nine thirty four because it should always be

123

00:13:08,885 –> 00:13:15,885

[kevin_martini]: home long first and then go find

your home okay okay okay let me talk

124

00:13:16,025 –> 00:13:21,185

[kevin_martini]: about this elephant that’s in the room

many good people were hurt during the housing

125

00:13:21,265 –> 00:13:26,734

[kevin_martini]: crisis in two thousand eight if you

are not directly impacted is likely that someone

126

00:13:26,794 –> 00:13:33,524

[kevin_martini]: you cared about was negatively impacted is

sad what happened during the housing crisis but

127

00:13:33,604 –> 00:13:39,553

[kevin_martini]: the events that caused it are not

present today sure the housing crisis caused the

128

00:13:39,633 –> 00:13:45,523

[kevin_martini]: great recession however the great recession did

not cause the housing crisis let me be

129

00:13:46,004 –> 00:13:56,492

[kevin_martini]: crystal clear recession does not housing crisis

today i am reminded by a quote from

130

00:13:56,852 –> 00:14:04,850

[kevin_martini]: warren buffet be fearful when others are

greedy and greedy when others are fearful i

131

00:14:04,890 –> 00:14:10,199

[kevin_martini]: would like to add get educated and

make an educated decision and was right for

132

00:14:10,339 –> 00:14:16,289

[kevin_martini]: you and your family based on the

facts not based on the headline or what

133

00:14:16,369 –> 00:14:22,623

[kevin_martini]: you heard the backyard barbecue there is

never a substitute for education and armed with

134

00:14:22,704 –> 00:14:29,862

[kevin_martini]: a proper knowledge you can find right

now it is time to be greedy because

135

00:14:29,963 –> 00:14:39,130

[kevin_martini]: i have confirmation more millionaires are made

when people are fearful inclosing home ownership is

136

00:14:39,311 –> 00:14:43,874

[kevin_martini]: not right for everyone and the only

way you can truly know if home ownership

137

00:14:43,954 –> 00:14:49,042

[kevin_martini]: is right for you and your family

is by searching for is not by searching

138

00:14:49,102 –> 00:14:55,070

[kevin_martini]: for homes on line or by driving

all over town to visit but houses the

139

00:14:55,230 –> 00:15:00,952

[kevin_martini]: first step is always a home loan

and then once you have clarity of the

140

00:15:01,032 –> 00:15:06,758

[kevin_martini]: cost and the certainty that you can

secure the proper financing for yourself and your

141

00:15:06,819 –> 00:15:12,174

[kevin_martini]: family then you can make an educated

decision if home ownership is right for you

142

00:15:12,756 –> 00:15:20,539

[kevin_martini]: and your family if not it’s totally

fine but you’re making a decision based on

143

00:15:20,719 –> 00:15:25,914

[kevin_martini]: education not got but if it’s right

for you then you can go find your

144

00:15:25,954 –> 00:15:32,423

[kevin_martini]: home being lager focused and with certainty

my name is kevin martini and my fellow

145

00:15:32,503 –> 00:15:37,171

[kevin_martini]: morgan strategist is logan martini and we

are here to help you if you have

146

00:15:37,251 –> 00:15:41,739

[kevin_martini]: questions about what was in this episode

episode one sixty one of the martini morte

147

00:15:41,799 –> 00:15:48,049

[kevin_martini]: podcast no we are here our number

is nine one nine two three eight forty

148

00:15:48,130 –> 00:15:55,314

[kevin_martini]: nine thirty four we both look forward

to help oh by the way our website

149

00:15:55,374 –> 00:16:02,366

[kevin_martini]: has fresh and real information about securing

the proper mortgage strategy along with relevant information

150

00:16:02,687 –> 00:16:09,994

[kevin_martini]: on what one needs to know if

they thinking of buying or need additional resources

151

00:16:10,676 –> 00:16:19,500

[kevin_martini]: check it out by going to w

w w martini mortgage group dot com thank

152

00:16:19,520 –> 00:16:24,213

[kevin_martini]: you for tuning into this new monthly

series called what the heck is going on

153

00:16:24,273 –> 00:16:29,904

[kevin_martini]: in october twenty twenty two and thank

you for sharing this episode with someone you

154

00:16:29,965 –> 00:16:33,941

[kevin_martini]: care about peace and blessings