If you are a first-time homebuyer or a repeat homebuyer, there are many things one needs to know and consider when buying a home. Certified Mortgage Advisor Kevin Martini and Senior Mortgage Strategist Logan Martini curated the Winter 2022 Martini Buyer Guide to simply explain the current real estate and mortgage markets plus vital information about buying a home and the process of getting a mortgage. The Winter 2022 edition of the Martini Buyer Guide has many informative articles that talk about things one needs to know about the current real estate and mortgage markets.

Winter 2022 Edition of Martini Buyer Guide

If you are buying real estate, if you are selling real estate, if you are refinancing a mortgage or if you work in the real estate arena then the Winter 2022 Martini Buyer Guide would be very helpful since it simply explains the current real estate and mortgage opportunity.

The Winter 2022 Martini Buyer Guide was curated to simply explain what is going on in the real estate and mortgage markets.

Logan Martini, Raleigh Mortgage Broker & Senior Mortgage Strategist

Contents of the Winter 2022 Martini Buyer Guide (things to know and consider when buying a home)

What is happening in the market?

With everything going on in the housing market right now, you may have a number of questions about what that means for you and your plans to buy a home. Here are three things that are likely top of mind for you.

- Why did Raleigh mortgage rates rise so much in 2022?

- What is happening with home prices in Raleigh?

- Should I buy a home in Raleigh today?

Expert insights for today’s homebuyers

If you want to buy a home today in Raleigh or anywhere for that matter, here are a few things experts say you should know about what to expect and why homeownership is so important.

Trends that are good news for Raleigh homebuyers

As the Raleigh real estate market has cooled but still remains strong, some of the intensity buyers faced during the peak frenzy of the pandemic has cooled too! Here are four trends that may be beneficial when you go to buy a home today.

- More homes to choose from

- Bidding wars have eased

- More negotiation power

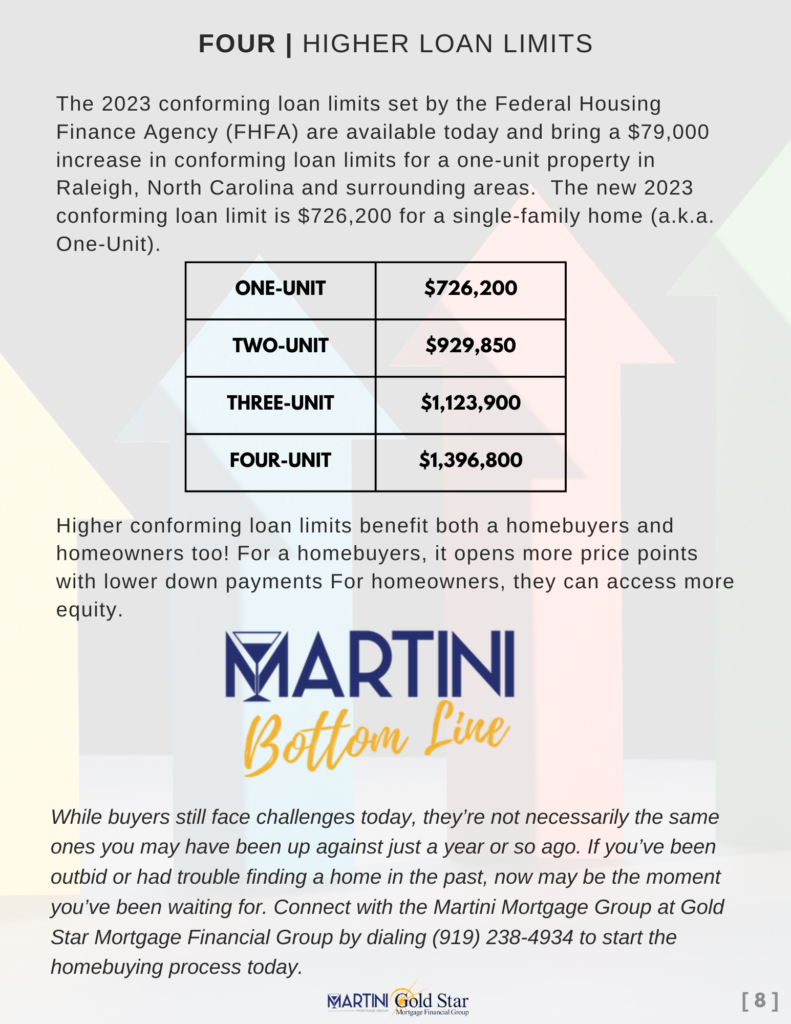

- Higher loan limits

2/1 Buydown

Increasing Raleigh mortgage rates are presenting some challenges and opportunities not just for first-time homebuyers but also to repeat homebuyers too! Leap over the challenges and into the opportunity with a creative mortgage strategy offered by the Martini Mortgage Group called a Seller Paid Buydown.

In most markets in North Carolina, especially in the Triangle, homebuyers will find that sellers are more willing to negotiate on price or other terms more than they have been in recent years.

Logan Martini, Raleigh Mortgage Broker & Senior Mortgage Strategist

5 traps to avoid when buying a home

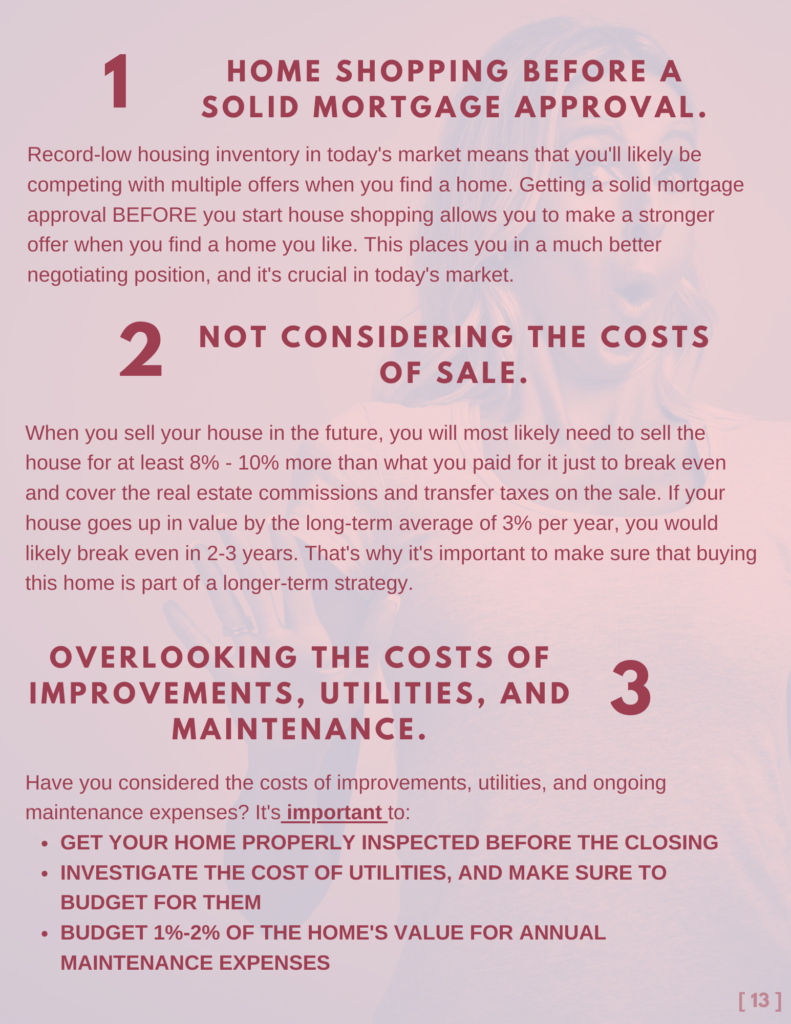

- Home shopping before a solid mortgage approval.

- Not considering the costs of sale.

- Overlooking the costs of improvements, utilities and maintenance.

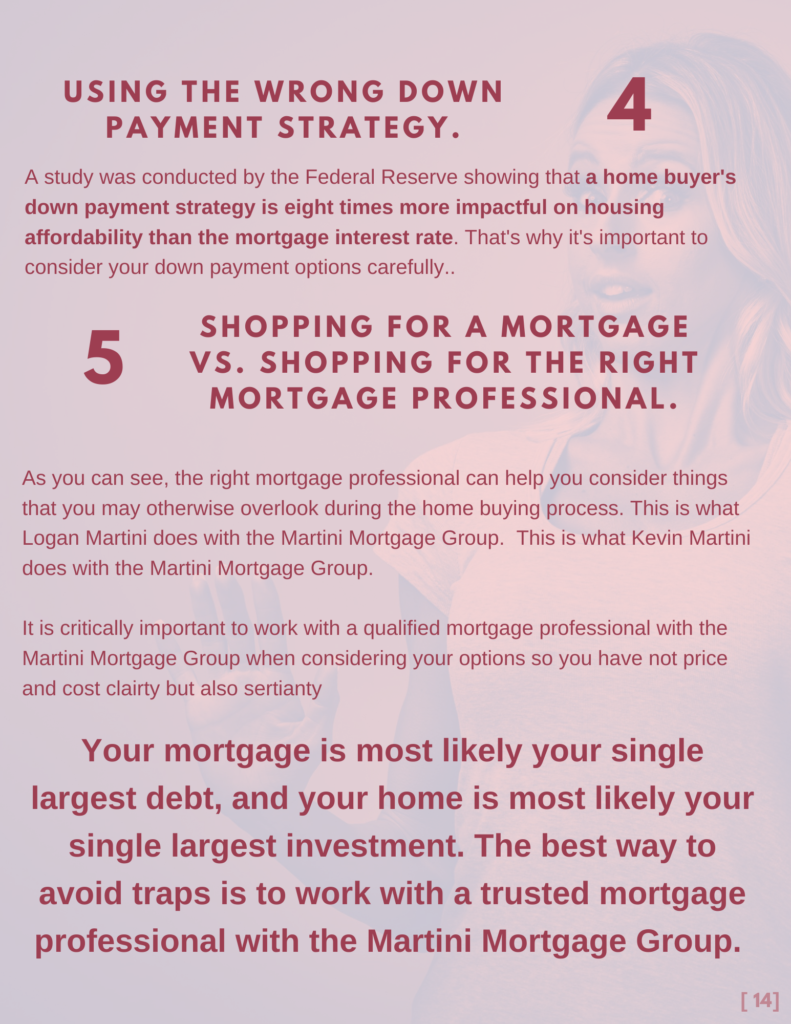

- Using the wrong down payment strategy.

- Shopping for a mortgage vs. shopping for the right mortgage professional.

Top reasons to own your home!

- Personal Expression

- Accomplishment

- Investment

- Comfort

- Family

- Community

- Privacy

- Stability

The non-financial benefits of homeownership

While you could see less competition and more room for negotiation, you may be wondering if now’s the best time to buy a home given Raleigh mortgage rates are higher than they were last year. While the financial aspects are important to consider, there are also powerful non-financial reasons it may make sense to become a homeowner. See the full article on page 16 of the Winter 2022 edition of the Martini Buyer Guide.

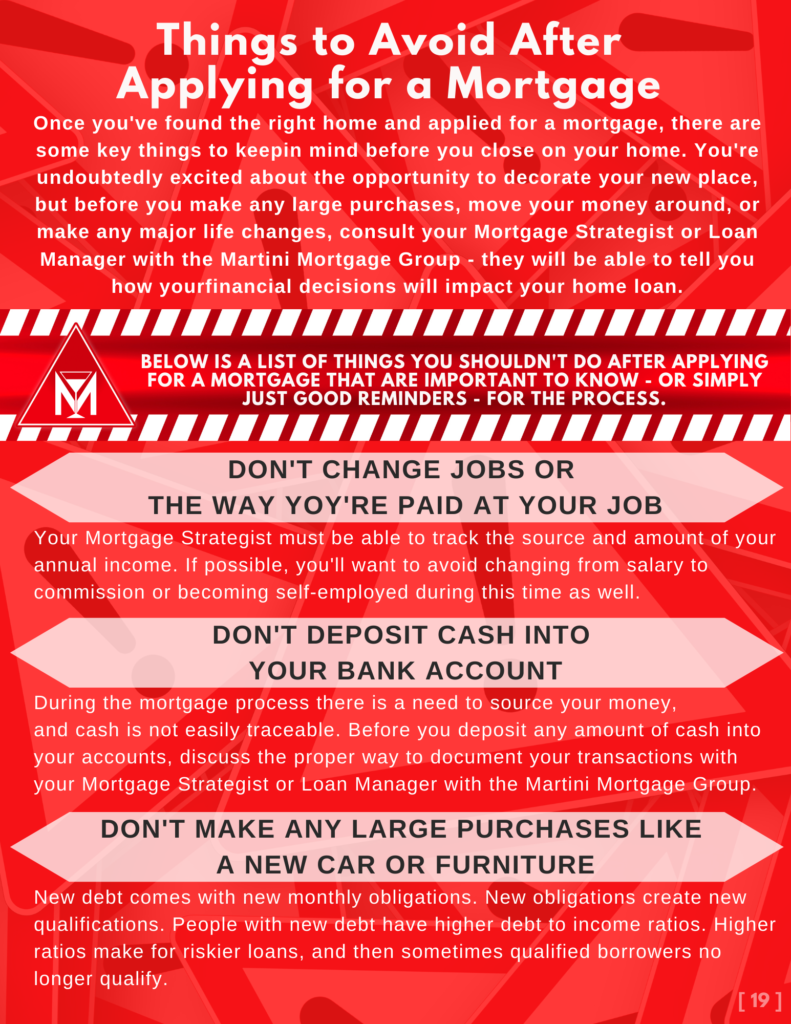

Things to avoid after applying for a mortgage!

Why buying a home makes better sense than renting

If there is a time to rent, that time is not now.

Kevin Martini, Certified Mortgage Advisor and Raleigh Mortgage Broker

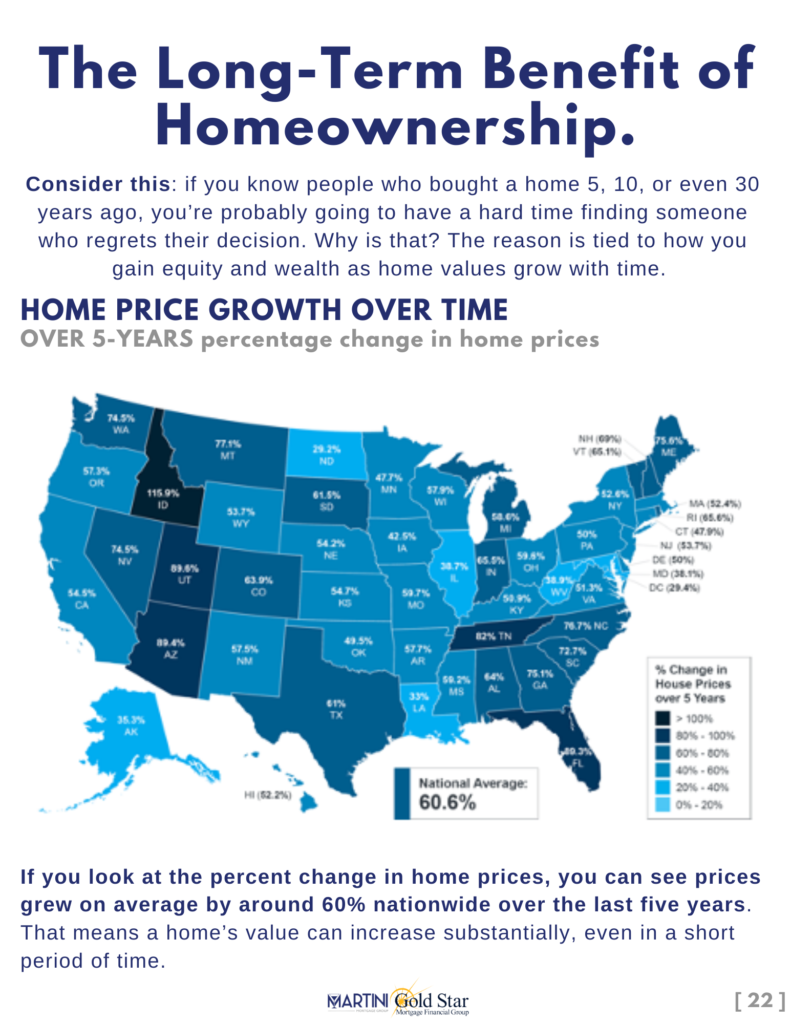

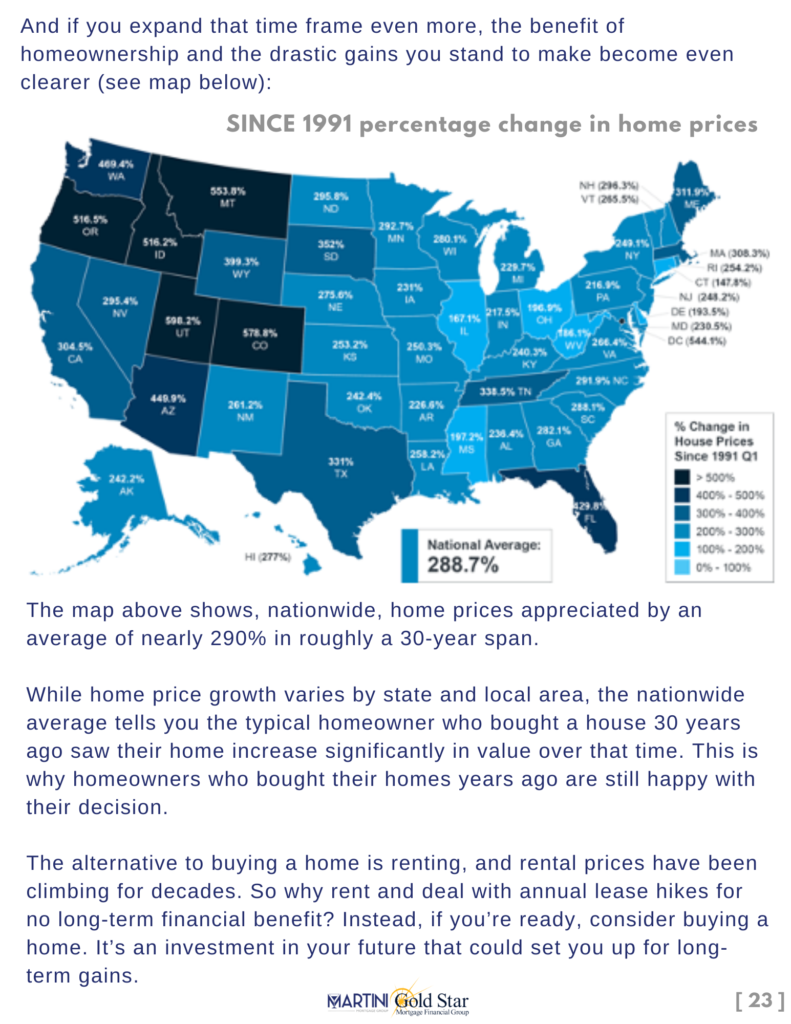

The long-term benefit of homeownership

Consider this: if you know people who bought a home 5, 10, or even 30 years ago, you’re probably going to have a hard time finding someone who regrets their decision. Why is that? The reason is tied to how you gain equity and wealth as home values grow with time.

Let’s chat…

I’m sure you have questions and thoughts about securing the proper mortgage with the lowest cost of borrowing and real estate process.

We’d love to talk with you about what you’ve read in the Winter 2022 Edition of the Martini Buyer Guide and help you on the path to buying your new home. Our number is (919) 238-4934 and we look forward to working with you.

Logan Martini

Senior Mortgage Strategist | NMLS 1591485

Logan@MartiniMortgageGroup.com

Kevin Martini

Certified Mortgage Advisor | NMLS 143962

Kevin@MartiniMortgageGroup.com