We are living in an unprecedented time, where the real estate market is experiencing shifts in sentiment among homebuyers and homeowners caused by an information crisis about housing. As a matter of fact, there is an immense demand for housing compared to supply, and this trend is not exclusive to Raleigh, North Carolina. Across the United States, there is a 3.8 to 5 million home shortage, which is not going to be resolved anytime soon.

This shortage is not a new phenomenon and has been a long-term issue that will take years, if not decades, to resolve. However, the shortage has created a unique opportunity for homebuyers to achieve a win-win-win situation. With the right strategy, homebuyers can take advantage of the market’s current stage and secure a sweet deal.

If you’re planning to buy a home in Raleigh, North Carolina, it’s important to understand the stages of buyer demand. These four stages are represented by a four-light stoplight. The red light represents weak buyer demand, orange represents limited buyer demand, light green represents good buyer demand, and the bright green light represents strong buyer demand.

Even though the current stage of buyer demand in Raleigh is in the red and orange zones, meaning there is a low to limited buyer demand due to slightly higher mortgage rates then have been seen in recent years. As a result, this is the perfect time for homebuyers to reduce competition and take advantage of a seller’s willingness to participate, which could make the deal more attractive. This also protects the homebuyer from paying a higher premium for the same home later.

Facts About Mortgage Rates

Mortgage rates live in the bond market and are not controlled by the Federal Reserve or the stock market. The inflation rate is the nemesis to the bond market, as it erodes the return of the bond. When inflation is under control, mortgage rates will drift lower. Currently, mortgage rates are in the high tides, but they are not predicted to reach double digits. Experts and pundits project that mortgage rates may start with a 4 by 2024-2025.

As a Raleigh Mortgage Broker, I know that this is the perfect time to take advantage of a seller-funded buydown. This temporary buydown provides a low rate today that can be refinanced to an even lower rate when mortgage rates fall in the future.

Certified Mortgage Broker and Raleigh Mortgage Broker Kevin Martini

Furthermore, understanding the stages of buyer demand and the unique opportunities they present, along with the current state of mortgage rates, is crucial for homebuyers in Raleigh. By securing a low rate today and taking advantage of the seller’s willingness to participate, homebuyers can protect themselves from paying a higher premium for the same home later, and potentially refinance the home loan to a lower rate once the rate enters the bright green zone.

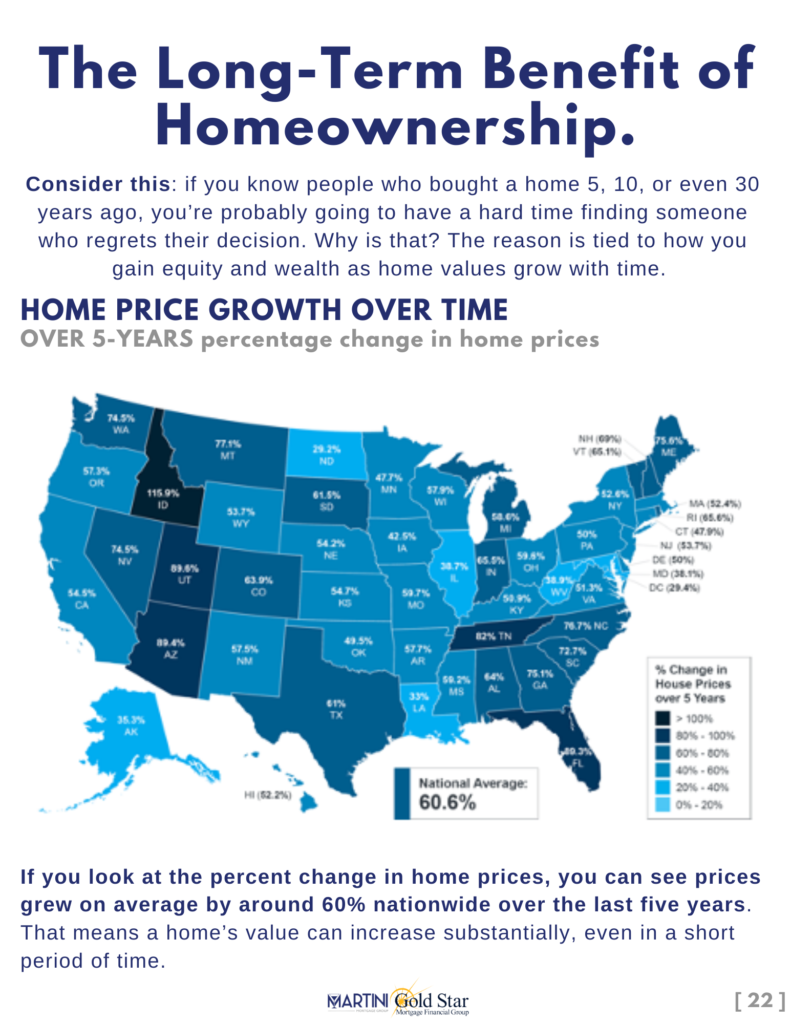

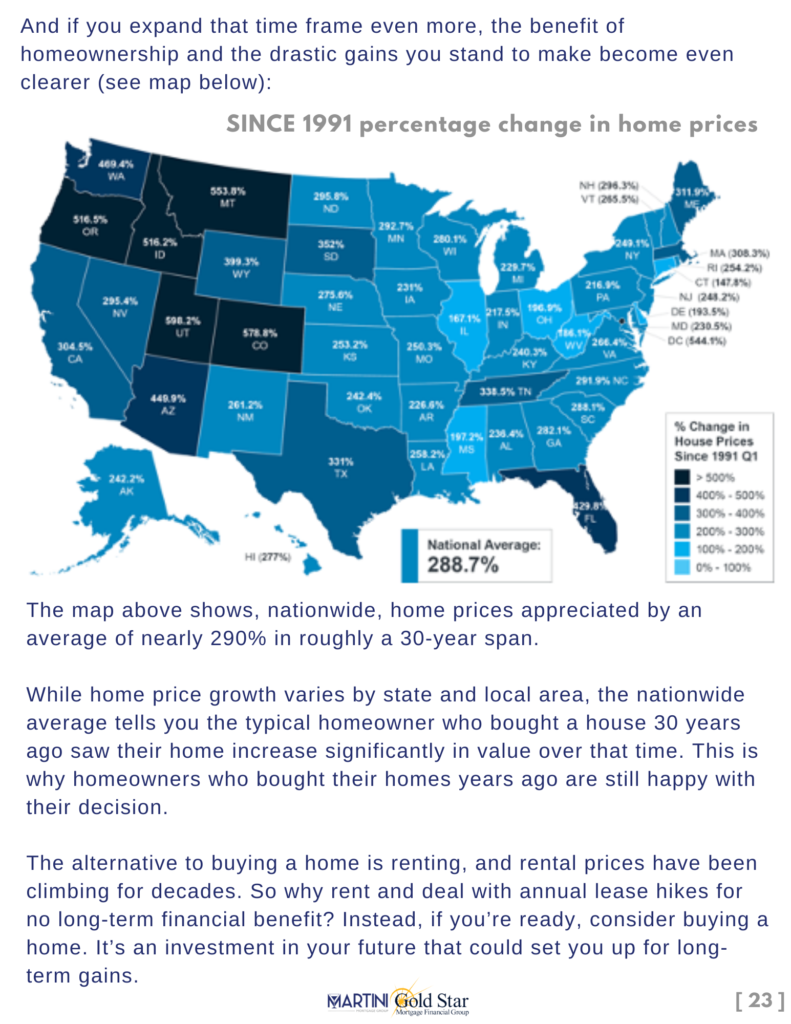

When considering buying a home, it’s important to remember that real estate is a long-term investment that goes up and makes higher highs over time. Although there may be moments of retracement, this period is just a time where real estate is recharging to make a higher high. North Carolina has experienced an average cumulative appreciation of 59.31% in the last five years and over 291% since 1991.

The pandemic was a once-in-a-generation event that provided unspeakable home loan rates and record-breaking home appreciation. However, this does not mean that homebuyers have missed out on an opportunity to secure a great deal. In fact, Kevin Martini said; “I can tell you that the best time to secure an epic mortgage rate was during the pandemic, but the next best time is right now.“

It’s important to understand that home values will go up over time due to the current shortage of supply and pure demand for housing. Although there may be moments of retracement, overtime real estate makes higher highs.

If you are thinking about buying a home in Raleigh, NC, or anywhere in the US, it is important to be aware of the current real estate market and understand the four stages of buyer demand. This knowledge will help you navigate the market and potentially maximize your advantage as a homebuyer.

Martini Mortgage Podcast, a Mortgage and Real Estate Podcast

In this episode of the Martini Mortgage Podcast, Certified Mortgage Advisor and Raleigh Mortgage Broker Kevin Martini discusses the current state of the real estate market and how homebuyers can use the four stages of buyer demand to their advantage. Martini explains that there is currently a shortage of homes available in the US, which is driving up home values. This shortage is not going to be resolved anytime soon, so it is important to be prepared and understand the market.

Martini explains that the four stages of buyer demand are represented by the colors red, orange, light green, and bright green. The red light represents weak buyer demand, which occurs when the mortgage rate is greater than 7 percent. The orange light represents limited buyer demand, which occurs when the home loan rate is lower than 7 but higher than mid 6’s. The light green color represents good buyer demand, which occurs when the home loan rate is lower than mid 6 percent. Finally, the bright green color represents strong buyer demand, which occurs when fixed mortgage rates start with a 5 or below.

It is important to understand these stages because they can impact the price you pay for a home. For example, in the red and orange stages, there is less competition among homebuyers, which means sellers may be more willing to negotiate and make the deal more attractive for you. In the light green stage, there is good buyer demand, so you may have more competition, but home prices are still reasonable. In the bright green stage, there is strong buyer demand, which means prices may be higher and sellers may have more demands, such as waiving inspections or paying over list.

Martini explains that understanding the four stages of buyer demand can help you time your home purchase to your advantage. For example, if you buy during the red or orange stage, you may be able to get a good deal on a home and lock in a baseline for your home purchase, protecting you from paying a higher premium for that home later. You can then refinance the home loan to a lower rate once the rate enters the bright green zone. By taking advantage of the red and orange stages, you can reduce your competition and potentially save money.

Martini also discusses mortgage rates and inflation, explaining that mortgage rates live in the bond market and are not controlled by the Federal Reserve or the stock market. The nemesis to a bond is inflation, which can erode the return of a bond and increase its yield to attract more buyers. Higher yield means higher mortgage rates. When inflation is tamed, mortgage rates will drift lower.

Martini’s insights can be particularly valuable to those interested in buying a home in Raleigh, NC. According to a recent report by Zillow, Raleigh’s housing market is currently considered “very hot,” with home values increasing by 10.8% over the past year. The median home value in Raleigh is currently $323,312, and Zillow predicts that home values will continue to increase by 11.5% over the next year.

If you are considering buying a home in Raleigh, NC or anywhere else in the country, it’s important to work with a knowledgeable and experienced mortgage broker who can help guide you through the process. The Martini Mortgage Group at Gold Star Mortgage Financial Group is a team of mortgage strategists who are dedicated to helping families achieve their dreams of homeownership.

One of the biggest advantages of working with a mortgage strategist with the Martini Mortgage Group is that they can help you navigate the complex mortgage process, including helping you understand your options and choose the right mortgage for your needs. They can also help you determine how much you can afford to spend on a home, which is critical in a tight housing market where prices are high and competition is fierce.

In addition to helping you with the mortgage process, the Martini Mortgage Group also provides the families they serve with valuable advice on the local real estate market, including insights on housing trends and the best areas to buy a home. This can be especially important in Raleigh, which is known for its strong real estate market and high demand for housing.

One of the best ways to get started with buying a home in Raleigh is to work with a mortgage strategist with the Martini Mortgage Group since they specializes in the area. They can help you understand the unique opportunities and challenges of the local market, as well as help you find the right home and mortgage for your needs.

At the end of the day, buying a home is a major investment that requires careful planning and consideration. By understanding the 4 stages of buyer demand and working with a knowledgeable mortgage broker, you can maximize your chances of getting a great deal on a home that you will love for years to come.

In conclusion, the current real estate market is characterized by high demand and limited supply, which has led to rising home prices and increased competition among buyers. However, by understanding the 4 stages of buyer demand and working with a knowledgeable mortgage strategist with the Martini Mortgage Group, you can take advantage of the unique opportunities of the market and find the right home at the right price with the right mortgage strategy.