For many of the families that the Martini Mortgage Group serves their homes the largest asset.

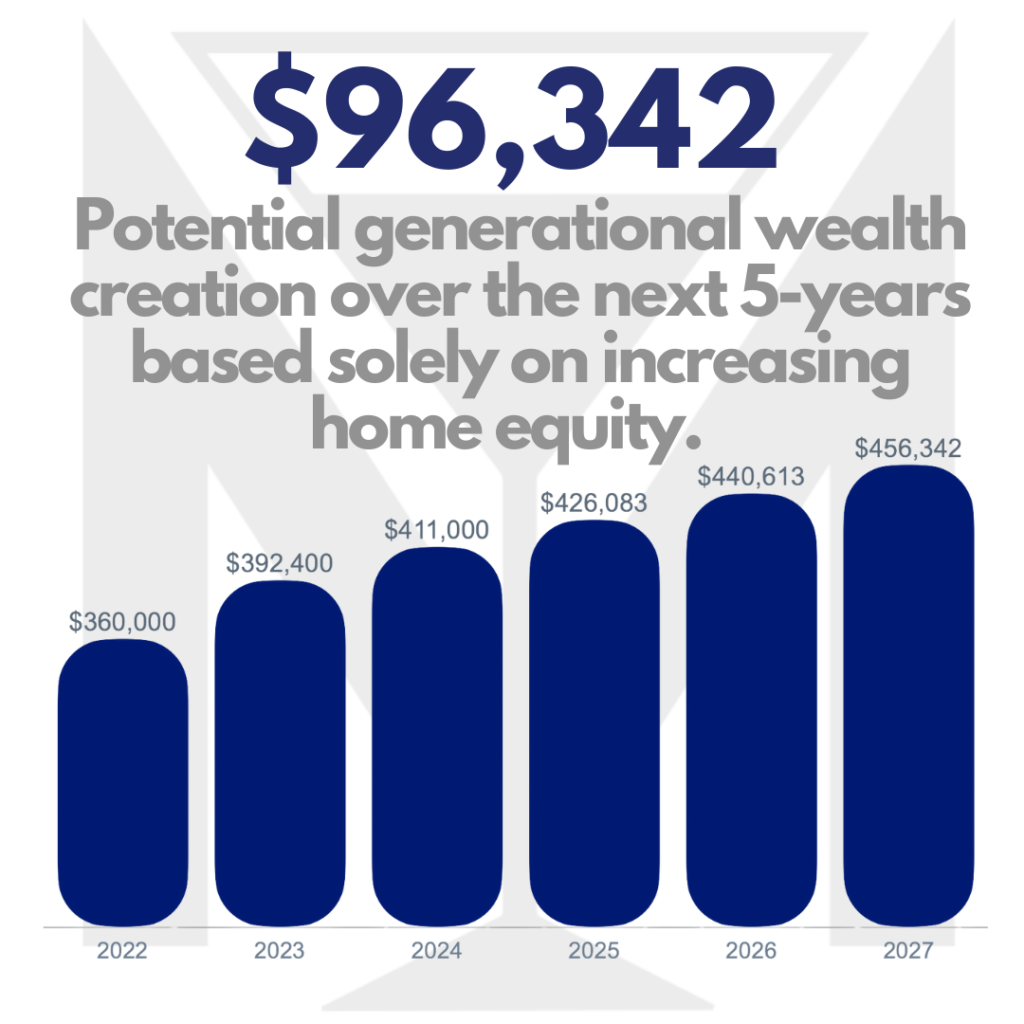

Knowing how your biggest asset is performing is not just nice, it is required! Having a clear understanding of your homes values can be useful to help determine if there are any next steps to take.

Homebot is a very powerful free tool offered by the Martini Mortgage Group to provide a quick snapshot of your equity in what is likely your largest asset, your home.

Kevin Martini, Certified Mortgage Advisor & Raleigh Mortgage Broker

Find out what your home is really worth with the Martini Mortgage Group home value tool.

Our data comes from the #1 market data company and it provides real-time market insight (i.e. a quick snapshot of the market, market indicators at-a-glance and market trends charts with historical view of home prices).

Benefits of knowing your home’s value by the Martini Mortgage Group

- Monitor your home’s value as it changes over time

- Track your ‘Tappable Equity’ (NOTE: Tappable Equity is the amount one can borrow and still preserve a 20% equity position)

- Manage you home’s value to assure it fits into your short and long-term financial strategy

Buy a Home with Confidence

If you are thinking of buying for the first-time or as a repeat homebuyer, unlock the your free report that highlights market temperature based on city and price point along with other powerful metrics. Here are just a few benefits to using the Martini Mortgage Group buyer portal:

- Know where and when to buy

- Understand your buying power

- Be ready and able to make your move

Oh by the way…

It is never too early to start to explore your homeownership options and you are not too late either. The first part of the homeownership journey is the loan and then after you have the certainty and being armed with price and cost clarity, the second step is to go find your home. The Martini Mortgage Group offers trusted advice with a frictionless digital mortgage process that provides certainty. To contact Mortgage Strategist with the Martini Mortgage Group simply call: (919) 238-4934.

LOGAN MARTINI

NMLS 1591485 | Senior Mortgage Strategist

Martini Mortgage Group at Gold Star Mortgage Financial Group, Corporation | NMLS # 3446 | 507 N Blount St, Raleigh, NC 27604

Logan@MartiniMortgageGroup.com

KEVIN MARTINI

NMLS 143962 | Certified Mortgage Advisor

Martini Mortgage Group at Gold Star Mortgage Financial Group, Corporation | NMLS # 3446 | 507 N Blount St, Raleigh, NC 27604

Kevin@MartiniMortgageGroup.com