How Much House Can I Afford in Raleigh NC in 2026?

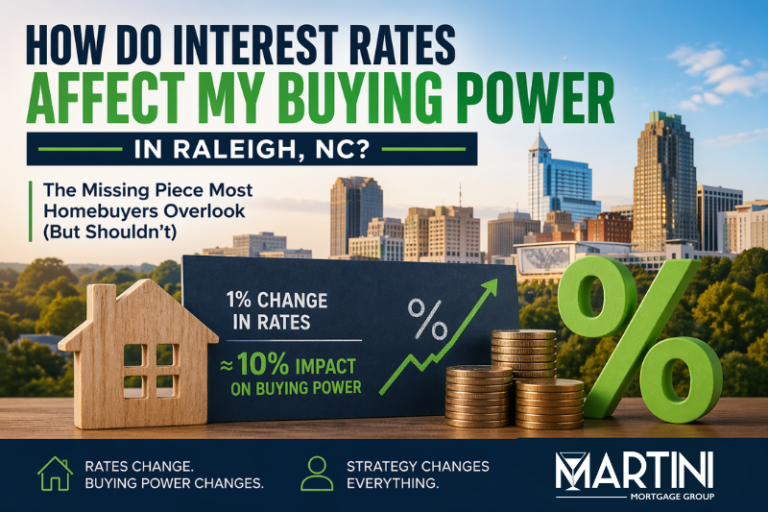

How much house can you afford in Raleigh, NC in 2026? Home affordability depends on four key factors: income, debt, down payment, and mortgage interest rates. In the Raleigh housing market, even small changes in interest rates can significantly impact buying power, often shifting affordability by as much as 10%. As rates and demand change across Raleigh, Wake County, and the Triangle, buyers must balance affordability with competition and timing. Understanding how these variables work together helps homebuyers make more strategic decisions—focusing on long-term financial positioning rather than simply chasing the highest approval amount.