When there is a conversation about a recession coming to Raleigh, North Carolina it is natural to be curious about what it means for mortgage rates and real estate values.

Episode 142 of the the Martini Mortgage Podcast with Certified Mortgage Advisor Kevin Martini is called Recession, Rates and Real Estate. In this special episode, Kevin Martini unpacks what experts believe will happen to Raleigh real estate and Raleigh home loan rates when there is a recession because there will be one — it is not a question of ‘if’, it is ‘when’ it will happen.

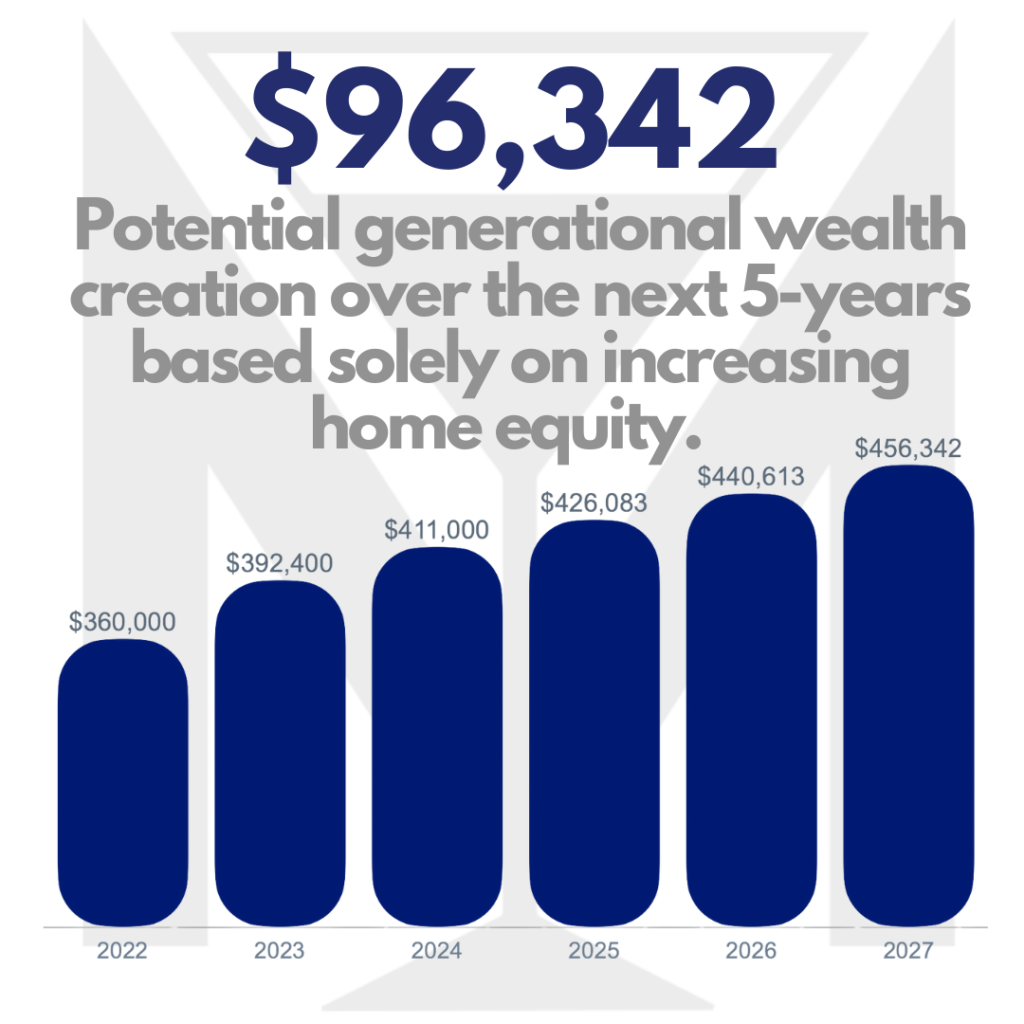

There is a lot of chatter recently about the thoughts of a recession coming to visit us. There are a lot of conversations about the upward movement in mortgage rates in 2022. And about the Federal Reserve, increasing the Fed funds rate and reducing their balance sheet. There is the reality that homebuyers are facing challenges finding the right place to call home. Welcome to Episode 142 of the Martini mortgage podcast. My name is Kevin Martini, and I’m a certified mortgage advisor with the Martini Mortgage Group, which is located in Raleigh, North Carolina, however, myself, along with a very talented crew of mortgage professionals, help families in all 100 counties in North Carolina, and pretty much in every state in the US to I’m calling this special episode of the Martini mortgage podcast recession rates and real estate recession rates and real estate. Oh, my, let us start with the recession. What is it simply put it is when there’s a decline in economic activity for two consecutive quarters, as reflected by the GDP and other economic indicators. GDP in the US dropped 1.4% In the first quarter of 2022. And this drop is an indicator of the potential recession coming. When will it come? I do not know. I do know this as it relates to a recession. It’s not if a recession is going to happen. It is when will a recession happen? And when the recession happens, what will happen to mortgage rates and real estate home values. When the recession rears its head. Historically, real estate performs very well. Since 1960, in the US, there have been nine recessions. In eight out of nine recessions, real estate values increased during the recession. The anomaly was during the Great Recession, which was during the housing crisis. Today, it is nothing like it was in 2008. Today, there were requirements to get a home loan. And back then the only requirement to secure a mortgage was to make sure you were breathing. Let me highlight before the Great Recession. If you had a low credit score with no job, you were getting a home loan, and in many instances you are able to get multiple home loans. It is critical to highlight to you the housing crisis led us into the recession, home values have not declined because of the recession. They declined because of the housing crisis. Let me say this again for the people in the back. The housing crisis led us into recession, home values did not decline because of the recession. They declined because of the housing crisis. Today, the home loans on the books are nothing like the ones that were on the books during the housing crisis. In addition, during the housing crisis, there was an excess inventory back then which amplified the situation. Recession does not mean reduction of home values. Also I feel obligated to highlight this deceleration of home values does not mean depreciation of home values. It is expected that values will not appreciate at the rate they have appreciated, hence deceleration. However, homes are still forecasted to appreciate. According to the home price expectation survey, home values over the next five years are projected to appreciate cumulative about 25% With the current inflation, some have the opinion that this cumulative 25% appreciation we’re five years is a conservative prediction. Here’s why.

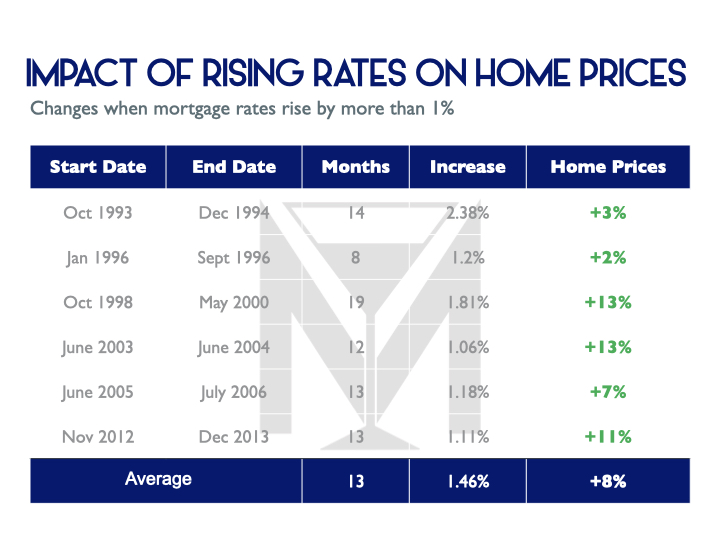

At the time of this recording of episode 141 of the Martini Mortgage Podcast, inflation is 8.5%. During periods of inflation, fixed assets like real estate perform very well since Owning a home is a hedge against inflation. Let me illustrate using what happened in the 70s During the 70s, consumer prices increased 7.1%. However homes appreciated 9.9%. Too far back. Okay. Let us look at the 90s. during that decade, consumer prices increased 3%. And homes appreciated 4%. When we look back at this period of time that we’re in today, it is my opinion, we will look back at 2022 as the good old days of real estate, we will right now are in a housing boom, not a housing bubble friends. Sure, this market has challenges and I understand it’s not easy out there. However, there are things that I can do as a certified mortgage advisor to put your offer in the pole position by allowing you to make a same as cash offer. Nothing very good for you is easy. If you want to be healthy, you have to exercise and eat right. It’s hard to exercise consistently and eating right is hard to Yes, buying a home for the first time or as a repeat homebuyer is not easy today. However, it’s easier if you follow the proper steps. The first step to homeownership is always the home loan. And the second step is to go find a home. And the third step is to make a same as cash offer with an approval package from the Martini Mortgage Group. I know their inventory challenges, and mortgage rates have drifted upward. And sure it would have cost you last if you purchased 12 months ago. But I’m reminding you that of this old Chinese proverb The best time to plant a tree was 20 years ago. The second best time is now for all those out there that fear our real estate bubble. Let me talk about inventory for a hot second. In 2007, there were 116 million households. Today there are 130 million households. Simply put, there are 14 million more households. And Freddie Mac estimates 3.8 million homes shortage of single family homes for those 130 million households. Let me compare this to the peak in 2007, where there were 3.7 million homes available for sale. And today there are under 900,000 homes for sale. Again, right now is an opportunity and is worth the effort. Even if mortgage rates are higher today, as compared to this time last year. Let us talk about mortgage rates and the Federal Reserve and what they are doing. As a primer. Mortgage rates are based on mortgage bonds, not on the federal funds rate. The Fed funds rate and mortgage rates are two different things. Remember when the Fed funds rate was zero, and many thought that meant mortgage rates were at zero? Obviously, you know that was not the case. Mortgage rates are based on mortgage bonds. When mortgage bond price moves downward to attract more buyers yield is increased. When yield is increased home loan rates rise between 1231 2021 and the end of April of 2022. The mortgage bond price has deteriorated nine point during that period of time. Why the move? Inflation is one of the key reasons for this move in mortgage rates. Again, home loan rates live in the bond market and the Nemesis to the to a bond is inflation. Inflation is high and high inflation negatively impacts mortgage rates. However, from a historical perspective, mortgage rates are still at a record level. Don’t believe me? Well, let

me share this fact with you. When my wife Ronnie and I purchased our first home, the rate for our mortgage was in the mid 90s. And that was not even for a fixed rate mortgage. If our first mortgage would have been a fixed mortgage, it would have been in double digits. What I am going to share now Next, it’s just literally going to blow your mind. What the Federal Reserve is doing today, based on history will improve mortgage rates over time. Raising the Fed funds rate is designed to lower inflation, lower inflation means improvement in home loan rates. Now, inflation did not just pop up overnight, it took time, so will take time for the Fed to get inflation under control. But they will. When inflation gets under control, mortgage rates should improve. You heard me correctly, I believe, rates will come down from the current levels. However, they will likely get worse before they get better, they will get worse because the Fed has a very large inventory of mortgage bonds they will be selling off. But when the dust settles, it should be a good thing. When will the dust settle? It is my gas best case by the end of 2022. But that may be too optimistic with the quantity of bonds they have to sell. And based on where inflation is today. But worst case, in the beginning of 2024. So should you wait to time the market? No. timing the market for mortgage rates is insane, because it’s essentially impossible to do. But even if you could wait it out for the pivot to lower mortgage rates, you will be paying a premium for the home since the home would have appreciated why you wait it. Here’s the fact you have three options today. Number one, call your folks and see if your bedroom is still available. Number two as you can keep renting and we all know that rents are up just under 20%. And then you’re subject to future increases. Or number three, take advantage of the housing boom, we are in today and lacking your housing costs. And no if I’m your mortgage advisor, I will monitor the markets for you after closing for the opportunity to lower your fixed housing costs with a refinance. In closing.

It is not if a recession will happen. It is when it will happen. During periods of recession, home values have done very well. Right now there’s not a housing bubble. Right now there is a housing opportunity. Right now mortgage rates are higher than they’ve been in the past several years. However, they are still very attractive and below the historic average. The Fed is working hard to control inflation, and they will but it will take time. Speaking of time, right now is it time to explore your homeownership options as a first time homebuyer or as a repeat homebuyer. Perhaps you are living in a house that you owe. But you and your family have outgrown it. Now is the time to upgrade. My name is kevin martini and I am a certified mortgage advisor with a martini Mortgage Group. I provide trusted advice with a frictionless process that offers great rates and certainty to you and your family. My number is 919-238-4934 Looking forward to connect. Stay safe out there and wishing you peace and blessings. Now it’s time for the disclaimer. This material has been prepared for marketing purposes only. This is not a loan commitment or guarantee of any kind. loan approval and rates are dependent upon borrower’s credit collateral financial history and program availability at time of origination rates in terms are subject to change without notice. The Martini Mortgage Group at PCL financials the division of celebrity Home Loans NMLS 227765 with a branch address of 507 North London street, Raleigh, North Carolina 27604 You can contact certified mortgage advisor and producing branch manager kevin martini NMLS NUMBER 143962 by calling the branch and that number is 919-238-4934. For a full list and more licensing information, please visit www NMLS consumer access that or or by visiting www.MartiniMortgageGroup.com equal housing lender