The MartiniFactor is produced by Raleigh Mortgage Broker Kevin Martini and it provides a glimpse of what happened last week in real estate and in the mortgage arena. In addition, it shares thoughts on what to keep on the radar for the week ahead.

Last week (4/22/2022) & this week (4/29/2022)

LAST WEEK IN THE REAL ESTATE & MORTAGE MARKETS

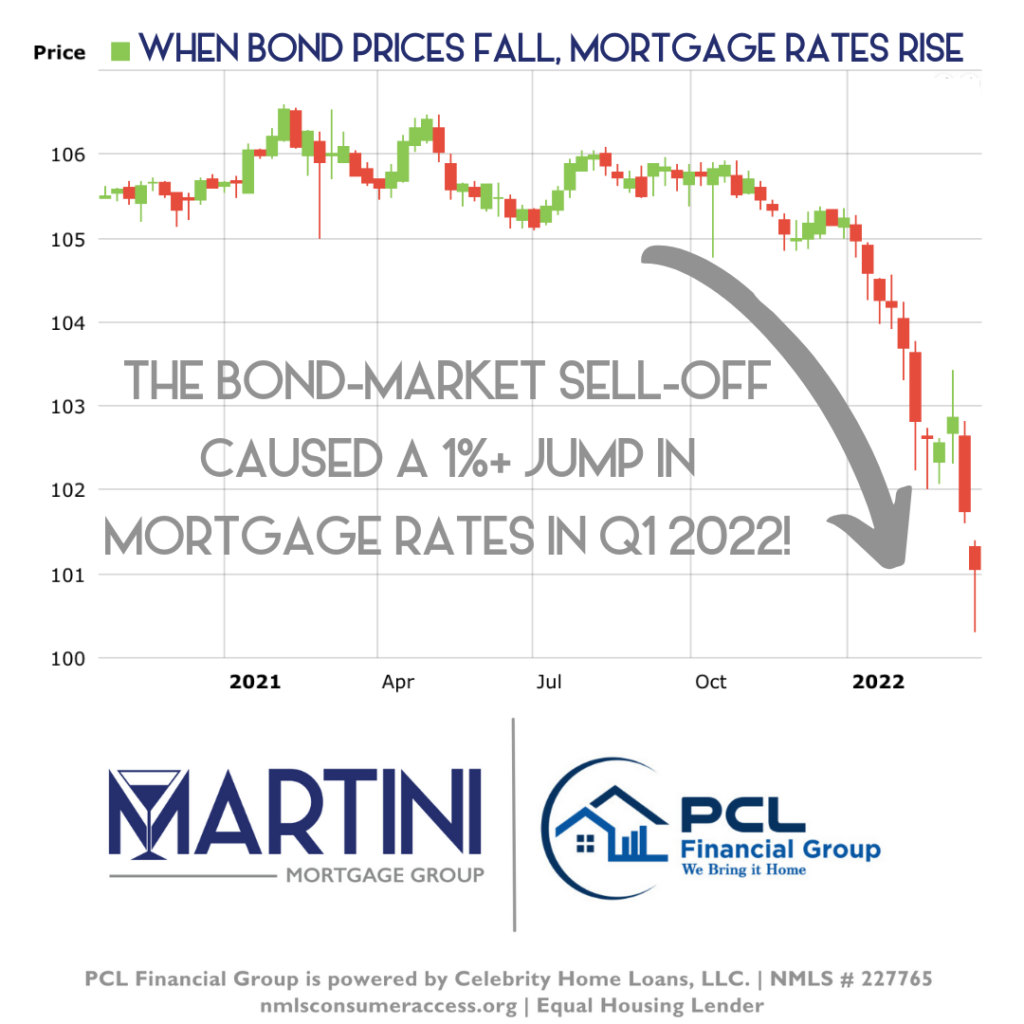

Last week we saw data relating to home sales; Month-Over-Month existing Home Sales were down 2.7% and Year-Over-Year Existing Home Sales were down 4.7%. This is the second month of decline for this metric however as you read this headline number, there may be concern however in you consider the current housing inventory and mortgage rates, the number was pretty good! Inventory is down 9.5% Year-Over-Year and mortgage rates have moved 1% plus in 2022. On the aggregate, the headline number does not tell the complete story considering the external factors (e.g. inventory & mortgage rates).

Some important numbers from last week:

The median home price was reported at $357,300, which is up 15% year over year. It is important to note, median home price is NOT the same as appreciation and ‘median’ is defined as the middle number is a sorted list of numbers. When there is a mix of sales prices, this number is distorted.

THIS WEEK IN THE REAL ESTATE & MORTAGE MARKETS

The big news this week that could disrupt markets will likely come from the G20 Meeting. Fed Chair Jerome Powell is scheduled to speak, and U.S. Treasury Secretary Janet Yellen is expected to attend the G20.

More news on the health of housing this week as the Case-Shiller Home Price Index , Federal Housing Finance Agency (FHFA) House Price Index. And Pending Home Sales data is released.

This week there will be an estimate for the 1st Quarter GDP along with critical inflation data which will be reported via Personal Consumption Expenditures index. Remember that Raleigh mortgage rates live in the bond market and the nemesis to bonds is inflation because inflation erodes the yield of a bond – the result is higher inflation means higher home loan rates.

THE MARTINI MORTGAGE GROUP BOTTOM LINE

Be prepared for more volatility and remember, right now, real estate and the current mortgage rate environment remains an opportunity. The Martini Mortgage Group is here to talk about what you have just read and here to help you on the path to buying you home. Contact the Martini Mortgage Group by dialing (919) 238-4934.

Kevin Martini | NMLS 143962 | Certified Mortgage Advisor and Producing Branch Manager | Martini Mortgage Group at PCL Financial Group (powered by Celebrity Home Loans, LLC NMLS 227765) | 507 N Blount St Raleigh, NC 27604 | (919) 238-4934 | www.MartiniMortgageGroup.com | Kevin@MartiniMortgageGroup.com | nmlsconsumeraccess.org | Equal Housing Lender