Your credit scores usually determine the price you pay for your money (mortgages, auto loans, auto leases, credit cards, business loans, personal loans, etc.). Perhaps the most significant part of your credit report is your credit score. For the purpose of mortgage, credit scores range from 350 to 850, with 850 being the best possible credit score, and 350 being the worst possible credit score.

Who Pulls Your Credit Will Determine Your Credit Score

The credit score you see may vary from what a lender sees and your credit score may vary between different debt being requested. This is because everyone has a unique credit score that represents their risk when applying for a new account based on what type of credit is being extended. Every industry has their own credit score model.

Different models are used to help a lender determine the credit risk for different type of debt. When securing an auto loan, the creditor is likely to use FICO (Fair Isaac Corporation) Auto Credit Score. When applying for a credit card, the creditor is likely using FICO 8 or VantageScore. When securing a mortgage, FICO Score 2, 4 and then 5 are used.

Credit Model & Scores Used When Applying For A Mortgage

There are three credit bureaus in the U.S. that collect information about you from your creditors. These bureaus then calculate a credit score based on that information. This means that you have three credit scores, one issued by each of the three credit bureaus:

- Equifax (model: FICO Score 5 or Equifax Beacon 5)

- Experian (model: FICO Score 2 or Experian/Fair Isaac Risk Model v2)

- TransUnion (model: FICO Score 4 or TranUnion FICO Risk Score 04)

Mortgage lenders typically order a tri-merged credit report when you apply for a home loan. The tri-merged credit report gives the lender information from all three credit bureaus. The lender typically uses your middle credit score when they evaluate your loan application.

(NOTE: YES, the score models used are older versions and newer credit score models are available however Fannie Mae and Freddie Mac guidelines require these older versions be used.)

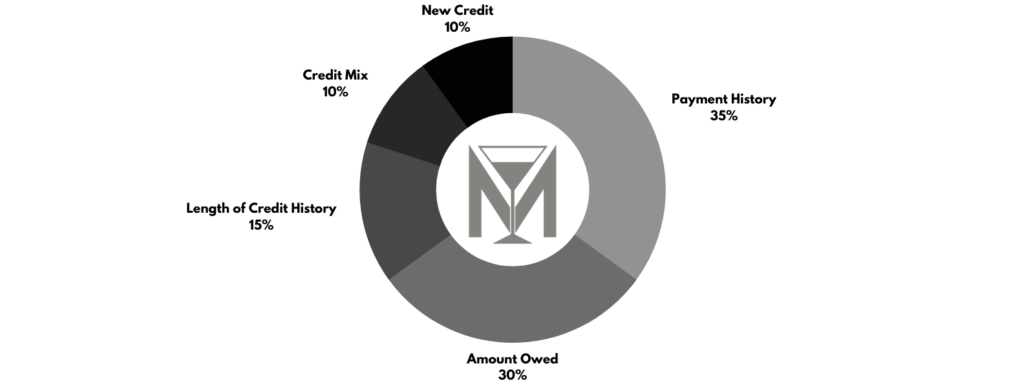

5 Factors That Determine Your Credit Score For Mortgage

Payment History has a 35% Impact on Credit Score for Mortgage

The biggest predictor of future payment behavior is past payment performance. Payment history makes up more than 1/3rd of the credit score for the purpose of mortgage.

Amount Owed has a 30% Impact on Credit Score for Mortgage

It is not just about the amount of the balance, it is about the balance as it relate to available credit. ‘Amount Owed’ is really the proportion of debt balances compared to the total available credit for that account.

Length of Credit History has a 15% Impact on Credit Score for Mortgage

Established credit accounts with a good track record. Time between older accounts and newer accounts.

Credit Mix has a 10% Impact on Credit Score for Mortgage

A well-balanced mix of credit accounts such as revolving credit, installment loans and mortgage.

New Credit has a 10% Impact on Credit Score for Mortgage

Newly established credit accounts put pressure on credit score until account performance can be established.

65% of your credit score is your payment history and balance-to-limit ratio.

Logan Martini